Personal Loan Optimizer

Find a smarter personal loan payment that balances projected interest savings, faster payoff, and monthly affordability.

Fynia uses advanced models to find your optimal monthly payment and show how extra payments change total interest and your payoff date.

Calculated from your inputs — actual lender results may vary. Not financial advice.

John Anderson

California

Personal loan

I assumed I’d need a huge payment increase to make a difference. Fynia showed me that even a small bump can cut interest dramatically.

Sarah Mitchell

Texas

Mortgage

An 8% increase in my monthly payment could reduce total interest by about 25%, that ratio was exactly what I needed to decide.

Michael Thompson

Florida

Personal loan

What I needed wasn’t ‘pay more’, it was knowing what’s worth it. The efficiency options made the trade-off between payment increase and interest savings instantly clear.

Emily Davis

New York

Business loan

I increased my payment by 14%, and the estimate showed around 26% less interest and 27 months faster payoff.

David Lee

Illinois

Auto loan

I stopped guessing. Fynia compared multiple scenarios and showed where the savings curve starts to flatten, so I could pick the smartest option.

Olivia Clark

Washington

Student loan

Fynia helped me pick a 9% payment increase that delivered roughly 14% interest savings—without overcommitting.

James Miller

Georgia

Personal loan

I cared more about reducing total interest than paying faster. Fynia highlighted options with the strongest interest reduction per extra dollar paid.

Sophia Garcia

Arizona

Mortgage

Comparing the scenarios showed me where extra payment stops being as efficient. I chose the option with 10% more payment for about 28% less interest.

Ethan Martinez

Nevada

Auto loan

I didn’t want the most aggressive plan, just the best ratio. The report helped me find the ‘sweet spot’ where a modest increase delivered the biggest impact.

Ava Rodriguez

California

Personal loan

With about 14% more per month, $37, I could save roughly $1200 in interest and finish 11 months sooner, nice.

Daniel Jackson

Ohio

Business loan

Seeing the percent increase in payment next to the percent drop in interest changed everything. I finally felt confident choosing a plan.

Isabella Walker

Michigan

Student loan

The report made it simple: 11% higher payment, 18% lower interest. That clarity helped me commit.

At Fynia, our mission is to help you estimate projected interest savings and payoff time—based on your inputs—by comparing more efficient monthly payment strategies. We focus on how each extra dollar you pay can work most efficiently to reduce your principal and shorten payoff time.

Higher payments don’t guarantee better results or higher payment efficiency. The sweet spot is the monthly payment that delivers the highest projected interest reduction per extra dollar paid—based on your inputs.

Efficiency represents the gap between the percentage increase in your monthly payment and the percentage reduction in total interest paid. The greatest difference between these two values is considered 100% efficiency. From this benchmark, all other efficiency levels are calculated, helping you achieve the optimal balance for saving on interest and shortening your loan repayment period. In the following link, you can find more detailed information about how Fynia works.

Fynia helps you find your optimal monthly payment and compare smarter payment options. See how these options can reduce total interest and reach your loan payoff date sooner—compared to your current payment—based on your inputs.

By accelerating your loan repayment and reducing your debt, Fynia helps boost your credit score. A stronger loan profile opens doors to better terms on future loans, credit cards, and financial opportunities, enhancing your financial well-being.

Fynia gives you a deep understanding of your loan conditions, empowering you to make informed decisions. Knowing exactly how interest, payments, and terms affect your debt allows you to take control and optimize your finances with confidence.

Fynia helps you test small payment increases to maximize projected interest savings with minimal cash-flow impact. For example, in some loans, a 5% increase can meaningfully reduce total interest and payoff time.

Find a smarter personal loan payment that balances projected interest savings, faster payoff, and monthly affordability.

Compare car loan repayment paths and identify the monthly payment with the strongest efficiency trade-off.

Explore how Fynia helps identify the maximum-efficiency mortgage payment to reduce long-term interest more intelligently.

Compare repayment paths and find a student loan payment that improves projected savings without overloading monthly cash flow.

Understand what a payoff optimizer does, how it differs from a simple calculator, and why comparing multiple payment paths matters.

See why even moderate payment increases can reduce total interest and improve payoff speed more than many borrowers expect.

Learn why faster payoff does not simply mean the highest payment and how to think about speed more intelligently.

Learn how to judge the trade-off between a bigger monthly payment, interest savings, payoff speed, and real affordability.

Basic

70%

Efficiency

The Basic option keeps your monthly payment increase to a minimum, offering modest savings in interest and a slight reduction in loan term. It’s a sensible starting point for those working with a tighter budget.

Standard

80%

Efficiency

The Standard option provides a balanced middle ground—more savings and faster payoff than Basic, but still very budget-friendly. It’s the best value choice for most users, combining meaningful efficiency with affordability.

Premium

90%

Efficiency

Premium increases your monthly payment modestly to achieve substantial interest savings and a shortened loan term. It offers a well-balanced upgrade in efficiency for borrowers seeking noticeable benefits without dramatic cost increases.

Ideal

100%

Efficiency

The Ideal option comes with a slightly higher monthly payment but delivers impeccable 100% efficiency, ensuring every cent is fully utilized to reduce both interest and your loan term.

Quick

90%

Efficiency

Quick accelerates your loan payoff with a higher monthly payment, offering notable time savings. However, it’s less efficient than Ideal—if fast repayment isn't essential, Ideal is the wiser pick.

Max

0%

Efficiency

The Max option sets the upper limit for monthly payments—beyond this point, additional increases result in negative efficiency. It serves as a clear warning: even if you can afford extra payments, going past this cap isn’t a smart strategy.

Key Facts

Loan Amount

$100,000

Interest Rate

15% annual

Current Monthly Payment

$1,264

Projected Results on Current Payment

Interest To Pay

$358,176

Total Repayment Amount

$458,176

Loan Term

30y 2mo

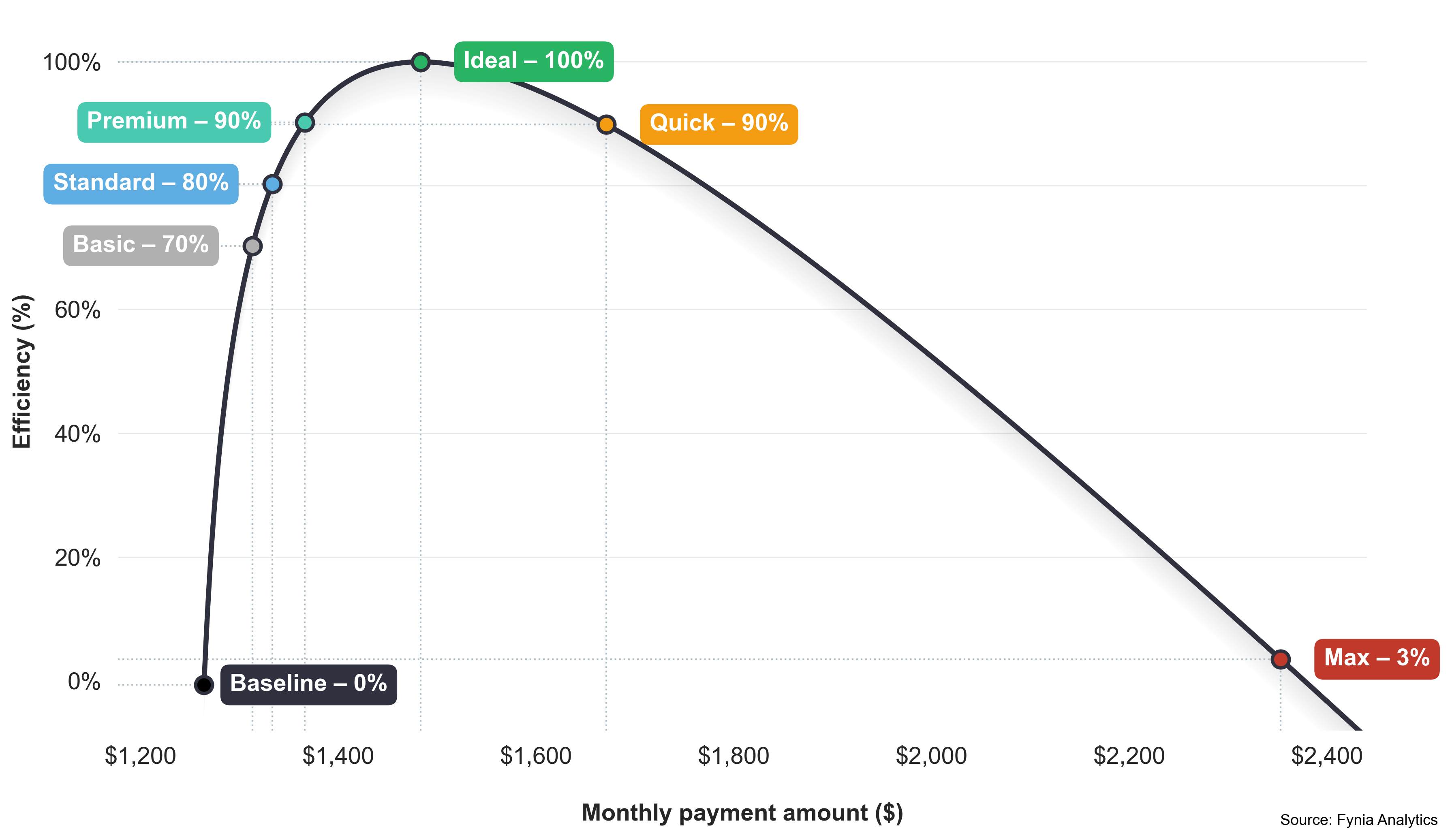

Payment efficiency is essential to making the most of every loan installment. The chart below is custom-built for your loan and shows how efficiency evolves with different monthly payment amounts. These suggested alternatives are recommended by Fynia to help you pay smarter, not harder. Each one designed to strike the best balance between monthly cost and total interest saved.

$1,313/mo

+$49 per month

3.9% increase

$220,991

Savings: $137,184

38.3% decrease

20y 5mo

9y 9mo shorter

32.3% decrease

$320,991

Increasing the monthly payment by 3.9%, following the Basic alternative, can lower interest expenses by 38.3% and reduce the loan term by 32.3%. This net benefit delivers 70% payment efficiency

GOOD

$1,333/mo

+$69 per month

5.5% increase

$197,918

Savings: $160,257

44.7% decrease

18y 8mo

11y 6mo shorter

38.1% decrease

$297,918

Increasing the monthly payment by 5.5%, following the Standard alternative, can lower interest expenses by 44.7% and reduce the loan term by 38.1%. This net benefit delivers 80% payment efficiency

VERY GOOD

$170,173

Savings: $187,003

52.2% decrease

16y 7mo

13y 7mo shorter

45.0% decrease

$271,173

Increasing the monthly payment by 8.1%, following the Premium alternative, can lower interest expenses by 52.2% and reduce the loan term by 45.0%. This net benefit delivers 90% payment efficiency

GREAT

$1,483/mo

+$219 per month

17.3% increase

$120,947

Savings: $237,229

66.2% decrease

12y 5mo

17y 9mo shorter

58.8% decrease

$220,947

Increasing the monthly payment by 17.3%, following the Ideal alternative, can lower interest expenses by 66.2% and reduce the loan term by 58.8%. This net benefit delivers 100% payment efficiency

PERFECT

$1,671/mo

+$407 per month

32.2% increase

$85,434

Savings: $272,742

76.2% decrease

9y 3mo

20y 11mo shorter

69.3% decrease

$185,434

Increasing the monthly payment by 32.2%, following the Quick alternative, can lower interest expenses by 76.2% and reduce the loan term by 69.3%. This net benefit delivers 90% payment efficiency

VERY GOOD

$2,353/mo

+$1,089 per month

86.2% increase

$43,511

Savings: $314,665

87.9% decrease

5y 1mo

25y 1mo shorter

83.2% decrease

$143,511

Increasing the monthly payment by 86.1%, following the Max alternative, can lower interest expenses by 87.9% and reduce the loan term by 83.2%. This net benefit delivers 0% payment efficiency

POOR

In this example, increasing the monthly payment by 17.3% reduces projected total interest by about 66% and shortens payoff time by about 59% (based on the inputs shown). Download the PDF to see the full breakdown.

How much do we charge?

$14.99

For each optimization, we charge $14.99, regardless of the loan’s characteristics. In many scenarios, optimizing your monthly payment can significantly reduce total interest and shorten payoff time—results vary by loan terms and lender rules.

How long does it take?

5-20 sec

In 5 to 20 seconds, you will have the optimization completed and your PDF report ready for download, which will also be sent to your email.

Each loan variable—amount, interest rate, payment periods, and installment—affects its behavior, making every optimization unique and tailored to your loan's specifics.

Each loan variable, amount, interest rate, payment periods, and installment, affects its behavior, making every optimization unique and tailored to your loan's specifics.

For a one-time payment of $14.99, you receive a report with multiple optimized payment options (e.g., Basic, Standard, Premium, Ideal, Quick, and Max) showing how different payment increases can reduce total interest and payoff time.

After checkout, you’ll receive an access token by email. The token is valid for 30 days and can be used once to generate an optimization report.

We only use your email address to deliver your token and purchase confirmation. We may store loan inputs (amount, rate, monthly payment, fees, and dates) and coarse location (country, and U.S. state) for aggregate analytics to improve Fynia. We do not collect names or ID numbers.

Fynia works best for standard installment loans where the payment schedule is predictable (e.g., mortgages, auto loans, student loans, personal loans, and many business term loans). If your rate or payment changes over time, results are estimates and may be less accurate.

No. Fynia provides estimates based on the information you enter. It is not financial advice and does not guarantee savings. Always verify final terms and amounts with your lender.

All sales are final. If you experience a technical issue that prevents token delivery or report generation, contact us and we’ll help resolve it (including reissuing a token when appropriate).

Email us at [email protected], we typically reply within 24 hours on business days.

Yes. Fynia is available worldwide. Checkout is handled by Lemon Squeezy, so availability may depend on payment processing in your region.

Check your spam/junk and promotions folders first. If you still can’t find it, email [email protected] from the same address used at checkout, and we’ll help you recover it.

You can add monthly fees to make the interest-savings estimate more realistic. Fees don’t change the optimization logic—they help estimate how much you could save by paying off the loan sooner.