Real Sample Result

Loan balance

$320,000

Annual interest rate

7.20%

0.60% monthly

Current payment

$2,218/mo

Current path term

28y 0mo

Joe Home Renovation Loan Example

See how Fynia compares payoff paths for a sample home renovation loan and highlights the payment path with the strongest Payment Efficiency.

This is a sample scenario. Results are estimates based on the loan inputs shown and lender terms.

Before vs Ideal

Joe's current path versus the strongest efficiency path

Fynia compares Joe's current payment against the six payoff paths in the report. In this sample, Ideal creates the strongest balance between extra monthly cash, projected savings, and payoff speed.

For +23.4% more each month:

45.1% less interest

39.9% shorter payoff

Joe's Ideal path is not the highest payment. It is the option with the strongest balance between extra monthly cash, projected savings, and payoff speed in this sample.

Six payoff paths

All six paths included in the same sample report

Each path represents a different monthly budget and tradeoff. The goal is not always to pay the most. The goal is to compare which path makes the strongest use of each extra monthly dollar.

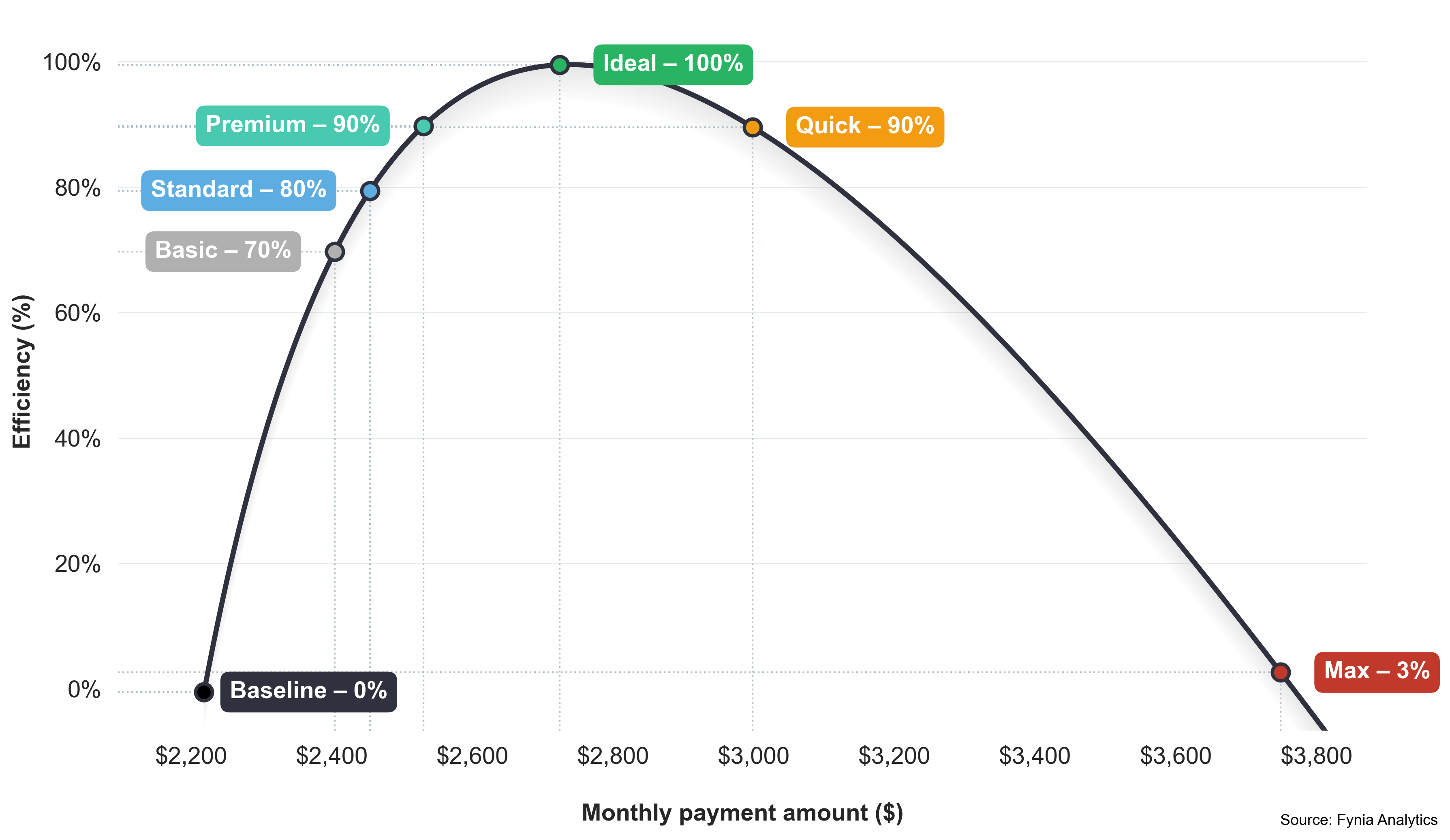

Basic

Lightest step upFor +8.4% more each month

23.6% less interest

20.2% shorter payoff

Payment increase vs. interest reduction

For +8.4% more each month, projected interest falls 23.6%.

That is 15.2 percentage points more interest reduction than payment increase.

A cautious step up for borrowers who want improved results with the smallest monthly increase.

5y 8mo faster payoff. Useful starting point, but still materially below Ideal on Payment Efficiency in this sample.

Standard

Balanced middle pathFor +10.6% more each month

28.0% less interest

24.1% shorter payoff

Payment increase vs. interest reduction

For +10.6% more each month, projected interest falls 28.0%.

That is 17.3 percentage points more interest reduction than payment increase.

A steady middle path for borrowers who can contribute a bit more without moving too aggressively.

6y 9mo faster payoff. A practical middle ground when you want a modest payment bump with much larger projected benefits.

Premium

Stronger progressFor +14.1% more each month

33.6% less interest

29.2% shorter payoff

Payment increase vs. interest reduction

For +14.1% more each month, projected interest falls 33.6%.

That is 19.6 percentage points more interest reduction than payment increase.

A stronger progress option that unlocks bigger savings without jumping into the most aggressive range.

8y 2mo faster payoff. Close to the strongest efficiency range while still requiring a controlled monthly increase.

Ideal

Peak efficiencyFor +23.4% more each month

45.1% less interest

39.9% shorter payoff

Payment increase vs. interest reduction

For +23.4% more each month, projected interest falls 45.1%.

That is 21.6 percentage points more interest reduction than payment increase.

The option where extra monthly cash, projected savings, and payoff speed create the strongest balance.

11y 2mo faster payoff. Ideal marks the strongest Payment Efficiency balance in this sample, not the highest payment.

Quick

Faster payoff focusFor +35.2% more each month

54.6% less interest

49.1% shorter payoff

Payment increase vs. interest reduction

For +35.2% more each month, projected interest falls 54.6%.

That is 19.4 percentage points more interest reduction than payment increase.

A faster-payoff path for borrowers who can commit meaningfully more monthly cash.

13y 9mo faster payoff. It moves faster, but the bigger payment already produces weaker efficiency than Ideal.

Max

Comparison capFor +69.0% more each month

69.4% less interest

64.3% shorter payoff

Payment increase vs. interest reduction

For +69.0% more each month, projected interest falls 69.4%.

That is only 0.4 percentage points more interest reduction than payment increase.

Max shows the upper end of the tested range. It may save more total dollars, but it is not necessarily the most efficient recommendation.

18y 0mo faster payoff. The results improve, but the payment jump is so large that this becomes a comparison cap, not the smartest default move.

Payment Efficiency

Why Ideal beats Max on efficiency in this renovation loan sample

Payment Efficiency compares how effectively each extra monthly dollar turns into projected savings and faster payoff.

- Ideal is the strongest efficiency balance in this sample - not the highest payment.

- Max marks where larger payments may create weaker returns, not the default recommendation.

Compare every path side by side

This is the deeper comparison layer for users who want the full picture. Review affordability, projected savings, payoff speed, and Payment Efficiency in one place.

| Metric | Baseline | Basic | Standard | Premium | Ideal | Quick | Max |

|---|---|---|---|---|---|---|---|

| Monthly payment | $2,218/mo | $2,404/mo+$186 · 8.4% increase | $2,454/mo+$236 · 10.6% increase | $2,530/mo+$312 · 14.1% increase | $2,738/mo+$520 · 23.4% increase | $2,998/mo+$780 · 35.2% increase | $3,749/mo+$1,531 · 69.0% increase |

| Projected interest | $424,245 | $324,115$100,130 savings · 23.6% less | $305,627$118,618 savings · 28.0% less | $281,626$142,619 savings · 33.6% less | $232,958$191,287 savings · 45.1% less | $192,610$231,636 savings · 54.6% less | $129,799$294,446 savings · 69.4% less |

| Payoff term | 28y 0mo | 22y 4mo5y 8mo faster · 20.2% shorter | 21y 3mo6y 9mo faster · 24.1% shorter | 19y 10mo8y 2mo faster · 29.2% shorter | 16y 10mo11y 2mo faster · 39.9% shorter | 14y 3mo13y 9mo faster · 49.1% shorter | 10y 0mo18y 0mo faster · 64.3% shorter |

| Total repayment | $744,245 | $644,115 | $625,627 | $601,626 | $552,958 | $512,610 | $449,799 |

| Payment Efficiency | 0.0% | 70.3%15.2pp comparison spread | 80.0%17.3pp comparison spread | 90.3%19.6pp comparison spread | 100.0%21.6pp comparison spread | 89.8%19.4pp comparison spread | 1.7%0.4pp comparison spread |

Download Joe's sample PDF report

The PDF shows the full sample report with payoff paths, projected results, and amortization schedules.

Find the payoff path that fits your numbers.

Run your loan analysis, compare all six payoff paths, and download your personalized payoff report.

One-time report. No subscription. Results are estimates based on your inputs.