The Power of Fynia in Action: Joe's Case

Joe has a home renovation loan with an outstanding balance of $320,000, at an annual interest rate of 7.2%. He is currently making monthly payments of $2,218. Joe wants to explore how he can optimize his repayment strategy to save the most money and pay off the loan faster.

Note: The following examples use January 2025 as a reference start date. Your analysis will use the specific date you enter.

Key Facts

Loan Amount

$320,000

Interes Rate

7.2% Annual

0.6% Monthly

Current Monthly Payment

$2,218

Projected Results on Current Payment

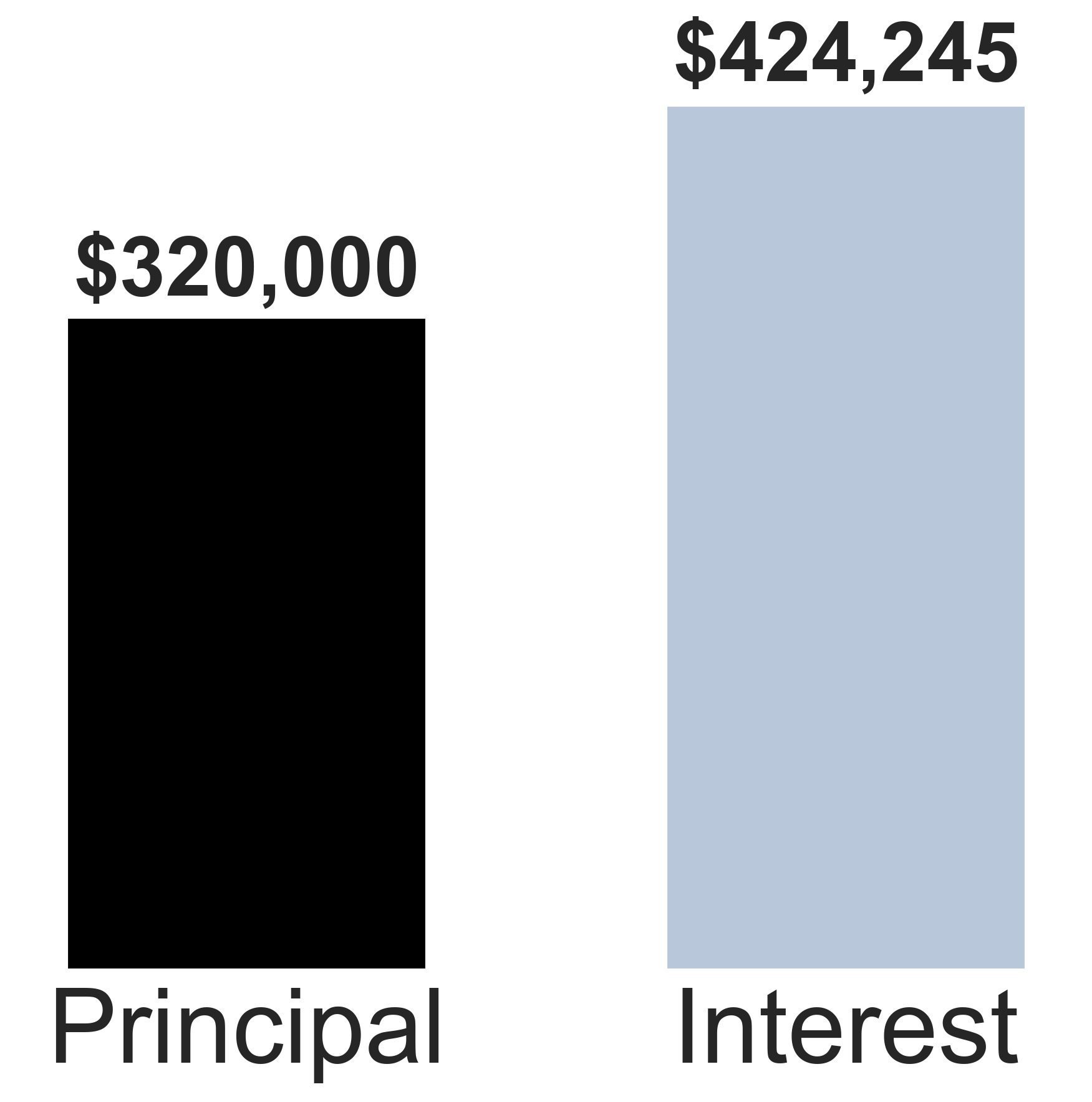

Interest To Pay

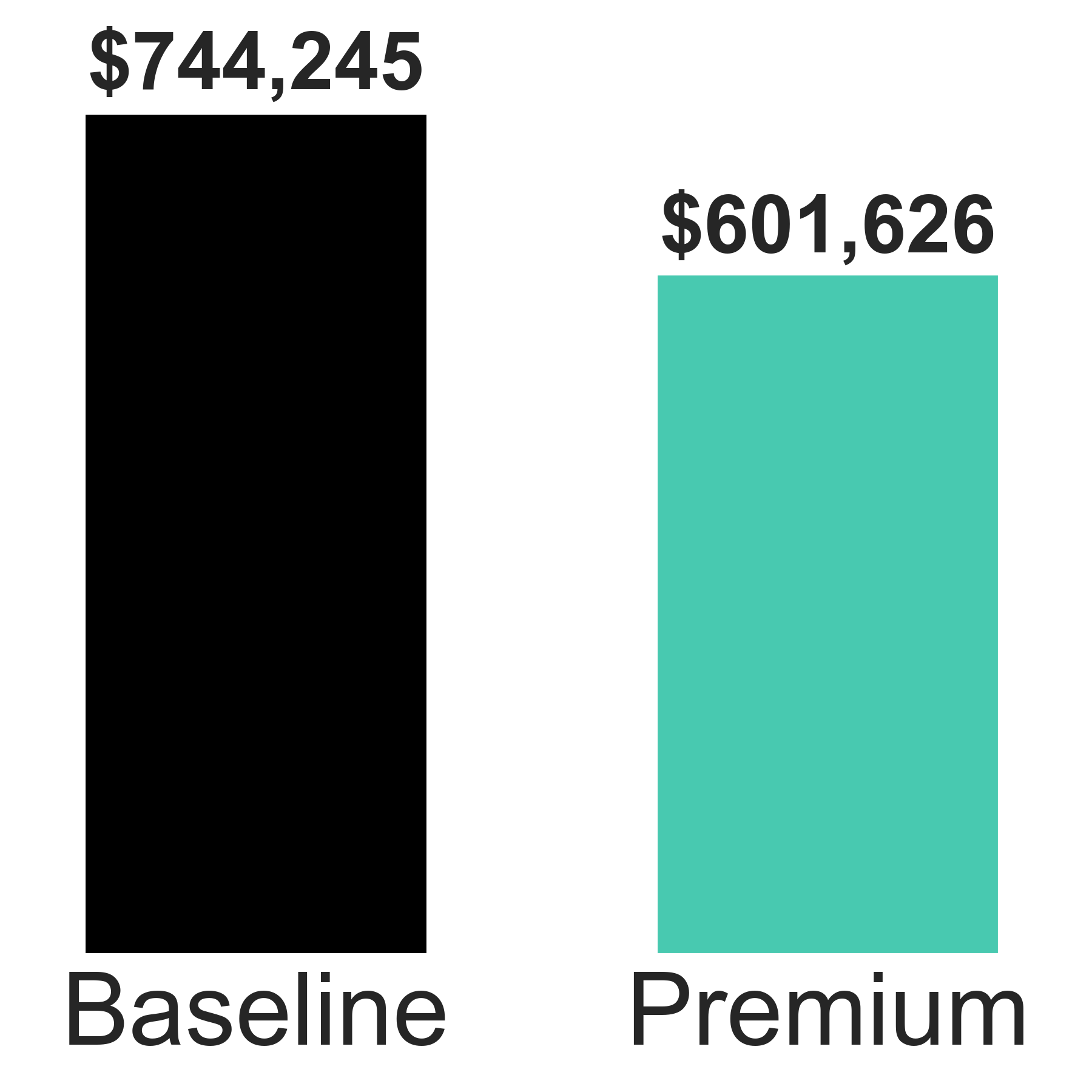

$424,245

Total Repayment Amount

$744,245

Loan Term

28y 0mo

Analysis of Joe's Loan

We organize each analysis into five key sections to make the information easy to follow. The example below reflects exactly how your own loan results will be shown, using Joe’s loan for demonstration.

1. Current Loan Overview

Take a quick look at your current loan details—see the key numbers that shape your financing today

2. Overview of Payment Alternatives

Get a quick snapshot of the alternatives Fynia has identified for you, with their key benefits in one place

3. In-Depth Option Analysis

Dive deeper into each alternative with detailed insights on the pros and cons of every option

4. Summary

A guide that steers you through selecting the best loan alternative for your budget

5. Download PDF Report

Download your full report in PDF format for convenient reference and future analysis

1. Current loan overview

Take a quick look at your current loan details—see the key numbers that shape your financing today.

Baseline Loan Conditions

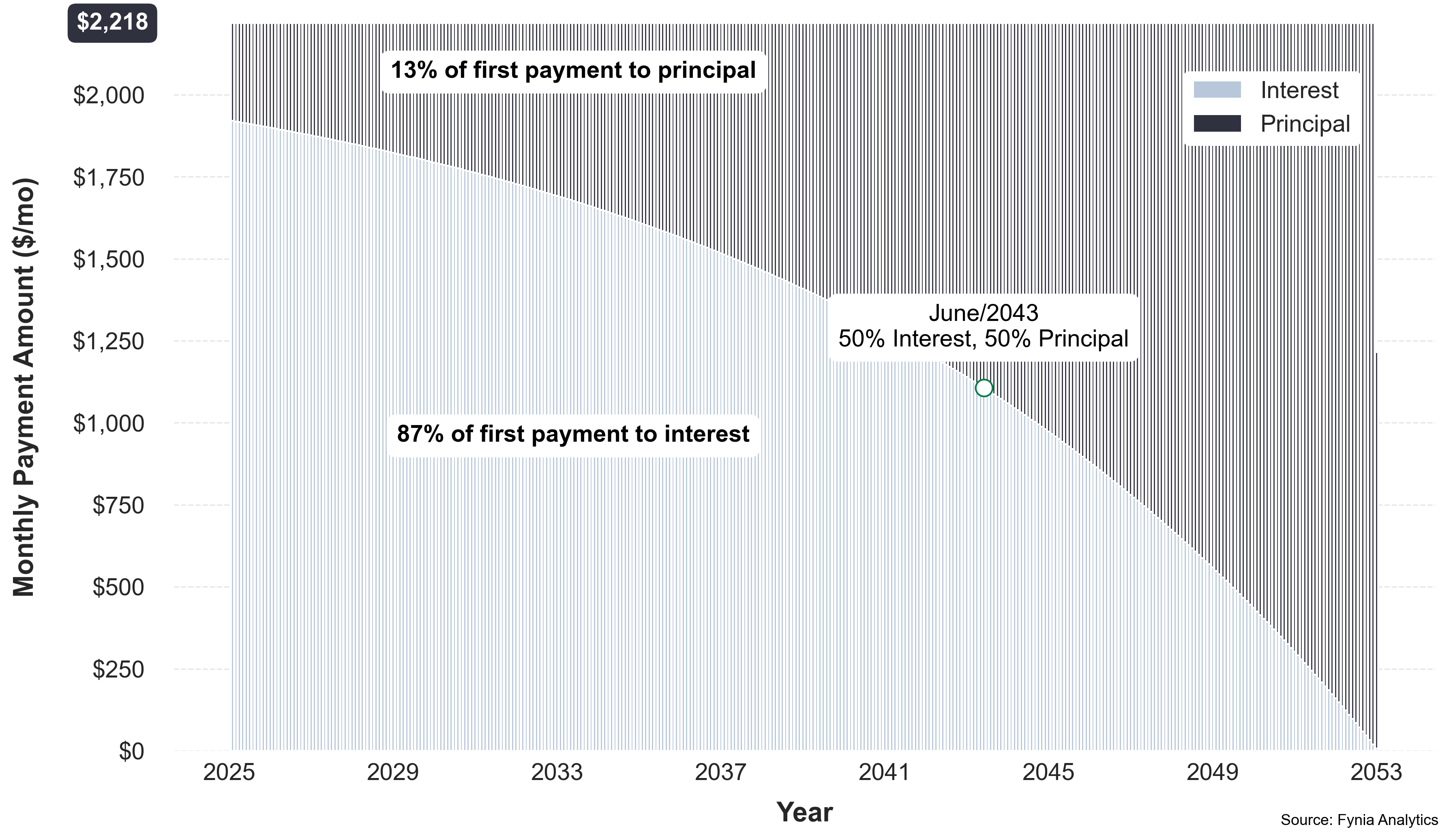

Monthly Payment

$2,218

Interest To Pay

$424,245

Loan-Term

28y 0mo

Total Repayment

$744,245

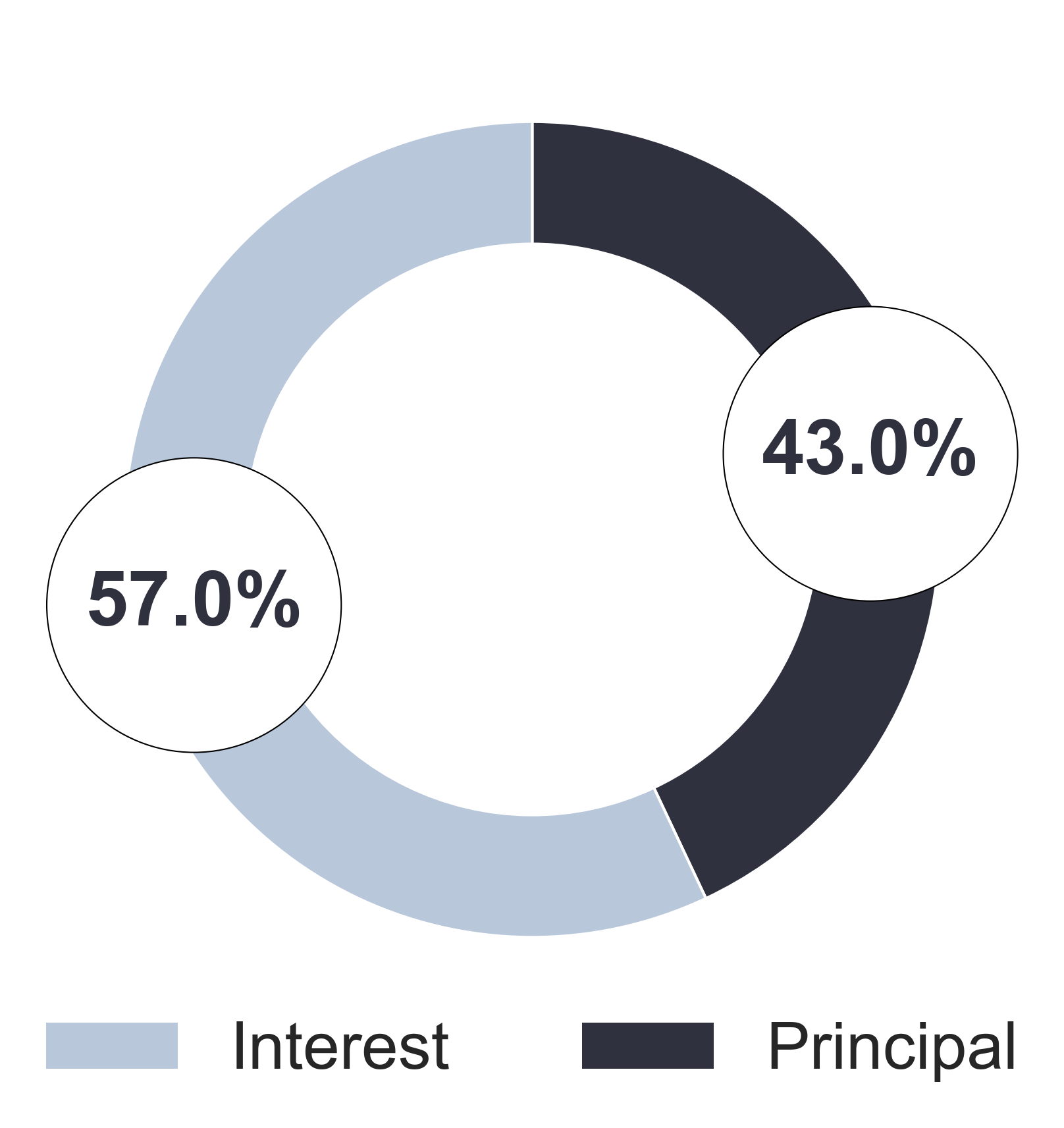

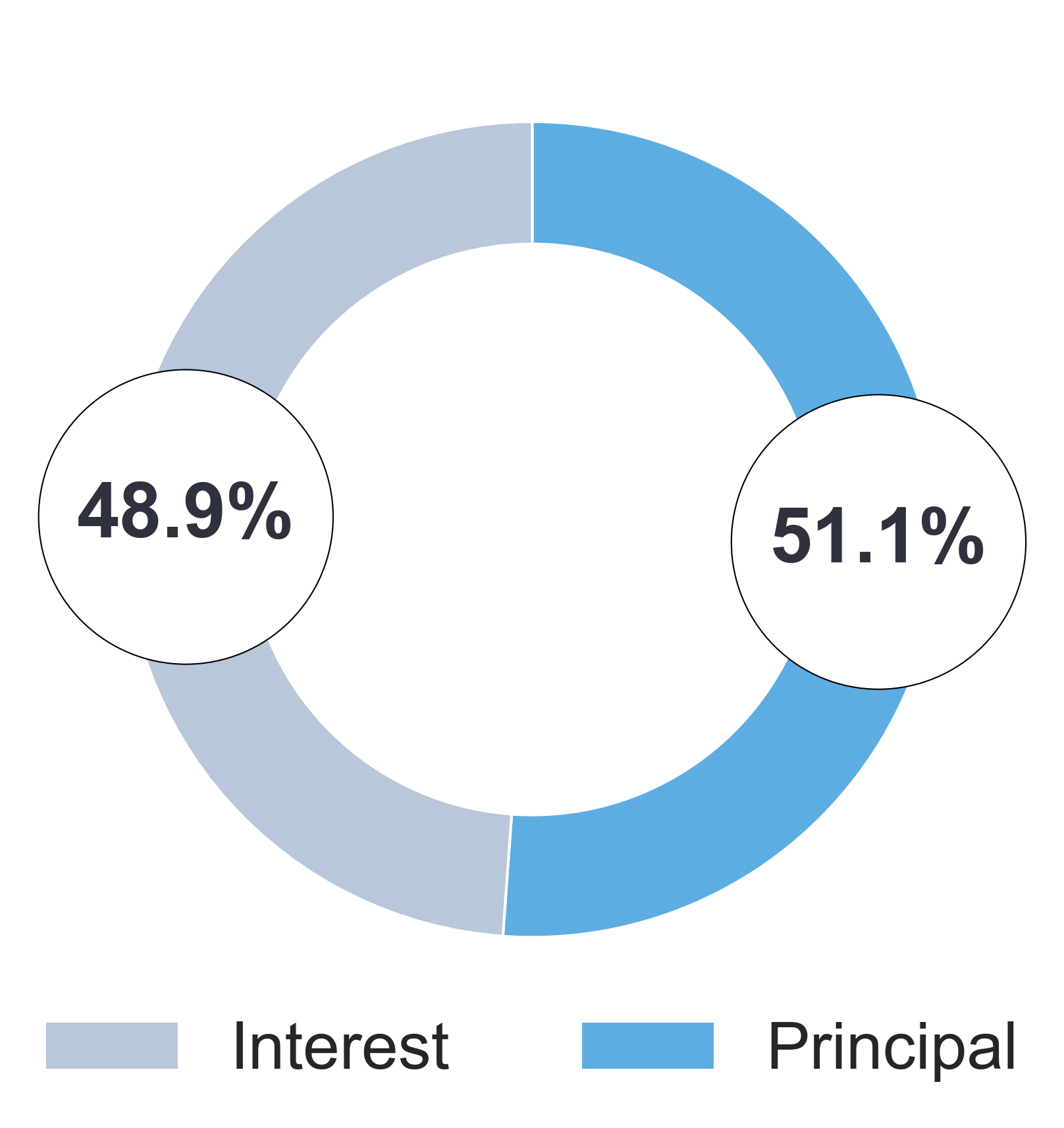

Total Payable Split

Payment Comparison

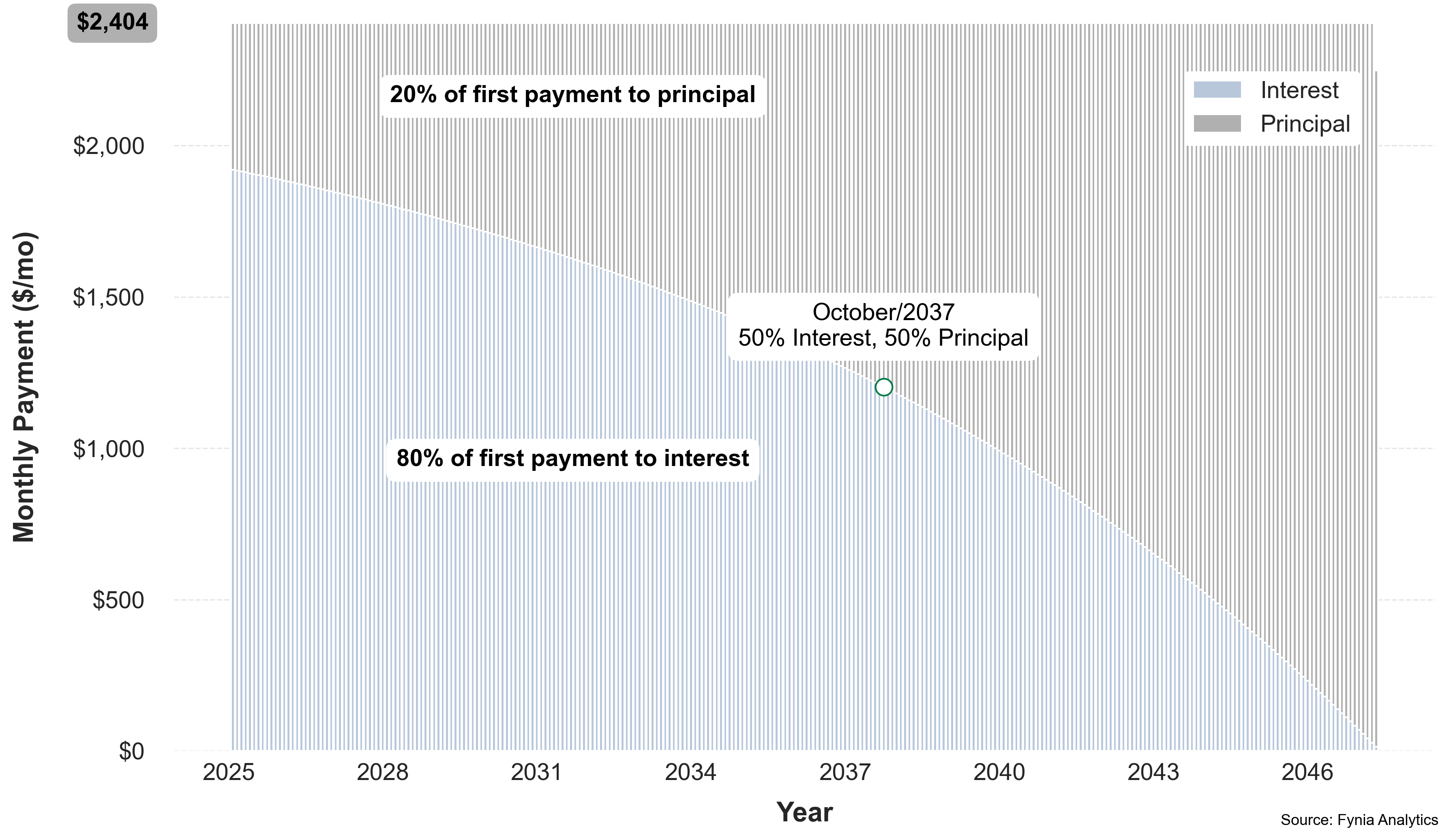

Monthly Payment Composition

Interest-Dominant Payment Period

65.5%

lower is better

Average Principal Contribution Percentage

43.0%

higher is better

Total Payment Ratio

232.6%

lower is better

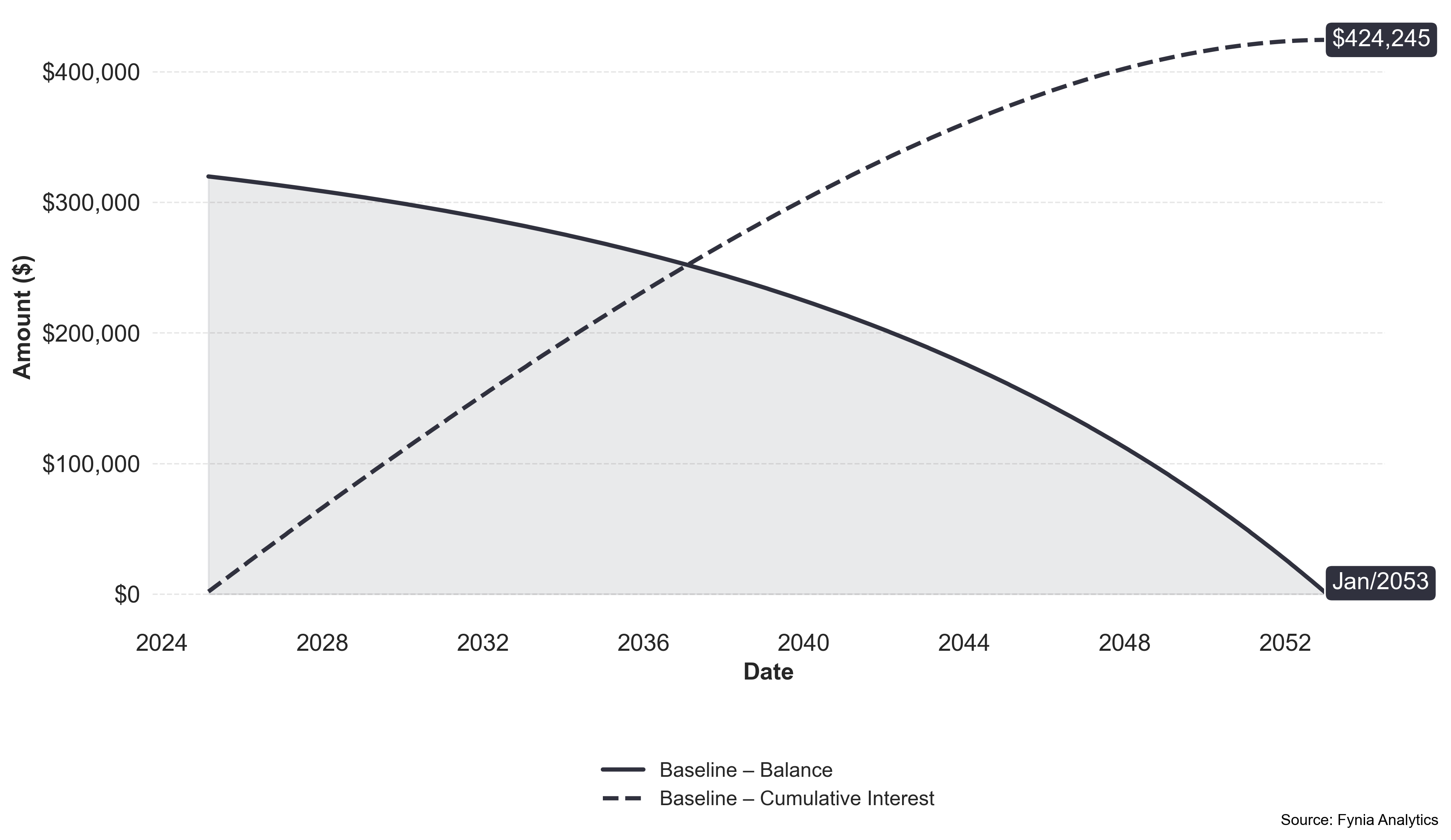

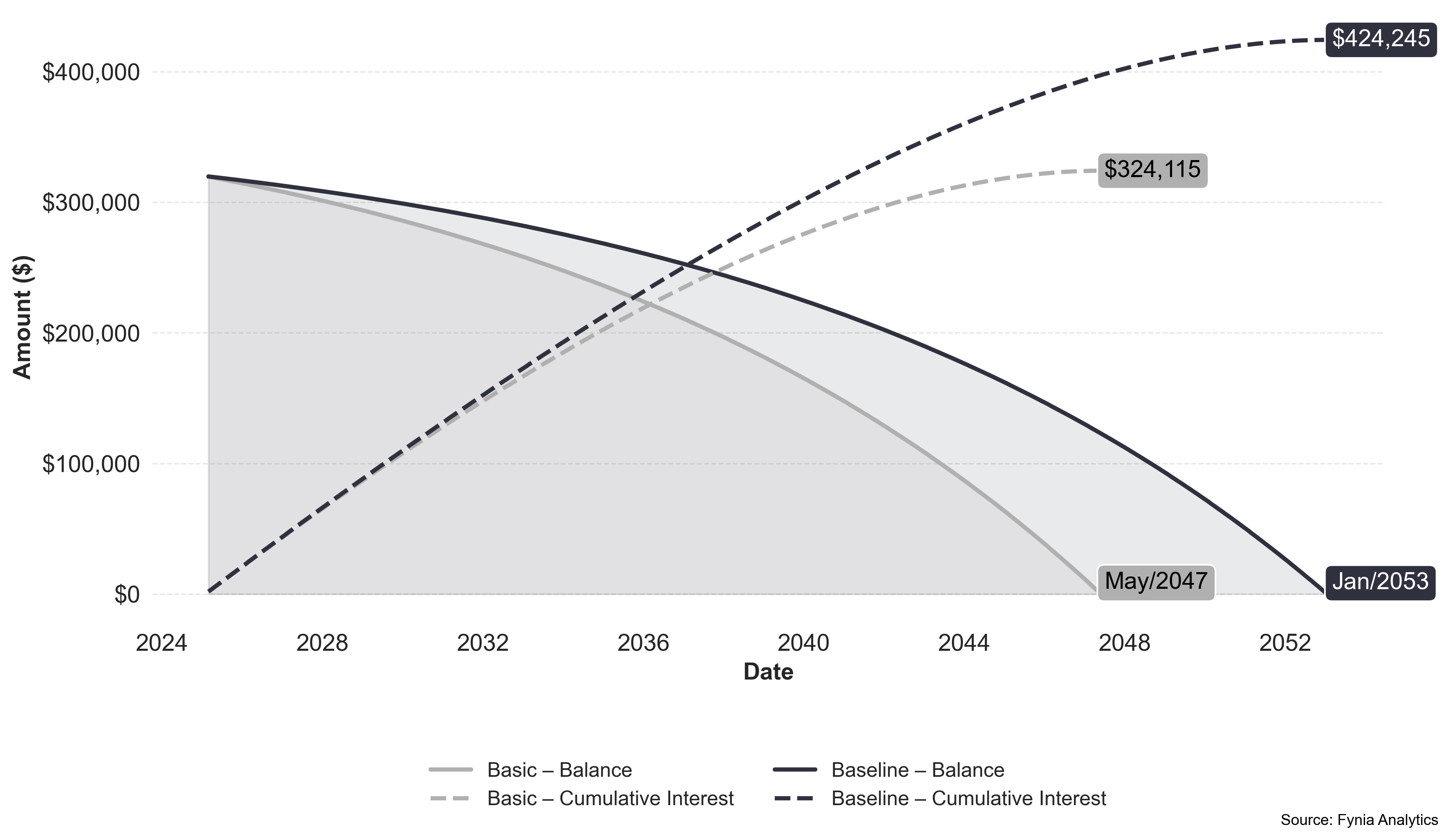

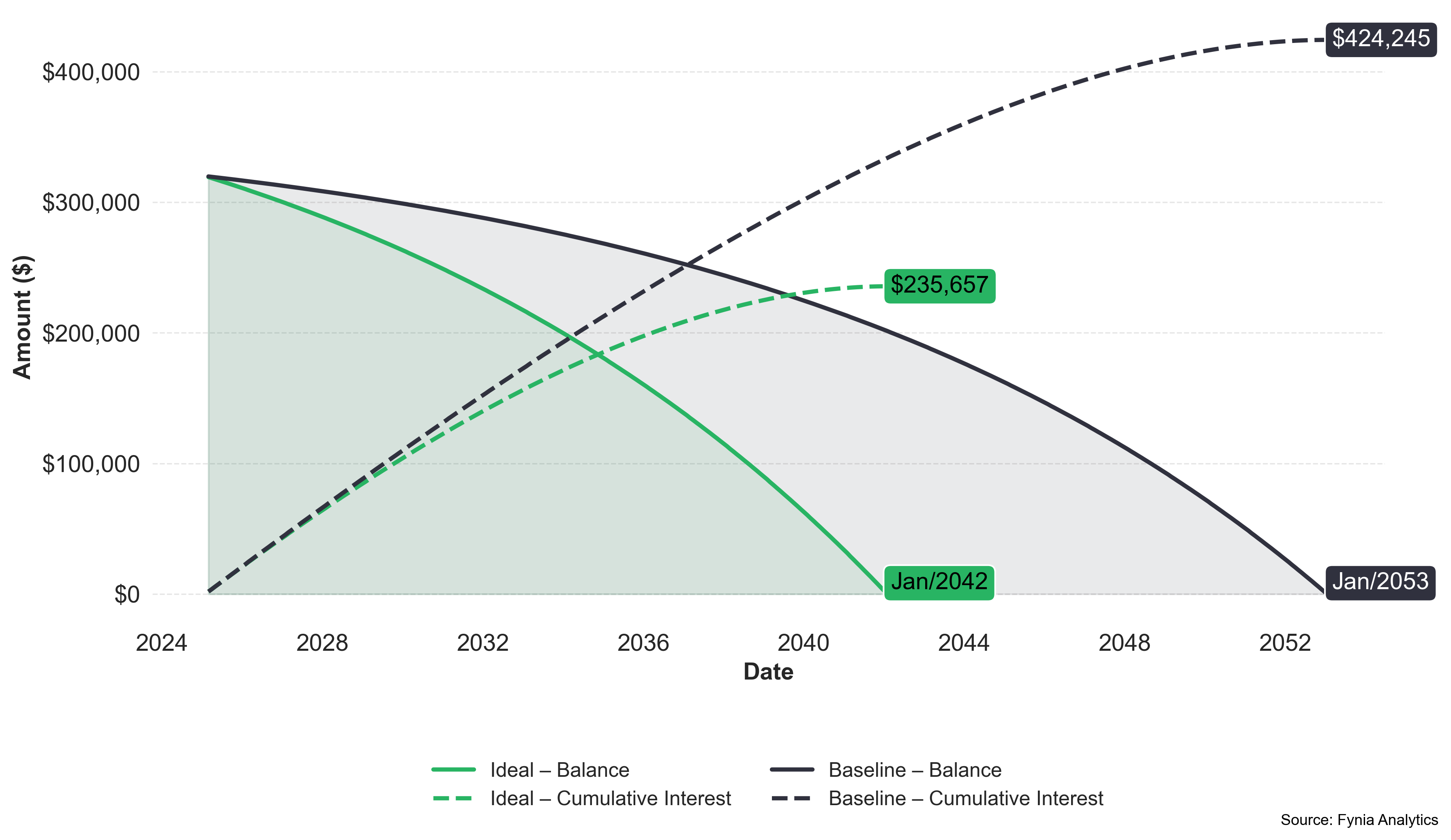

Balance And Cumulative Interest

50% of Balance Repaid

June/2043

Final Loan Payment Date

January/2053

Final payment (last installment)

$1,215.44

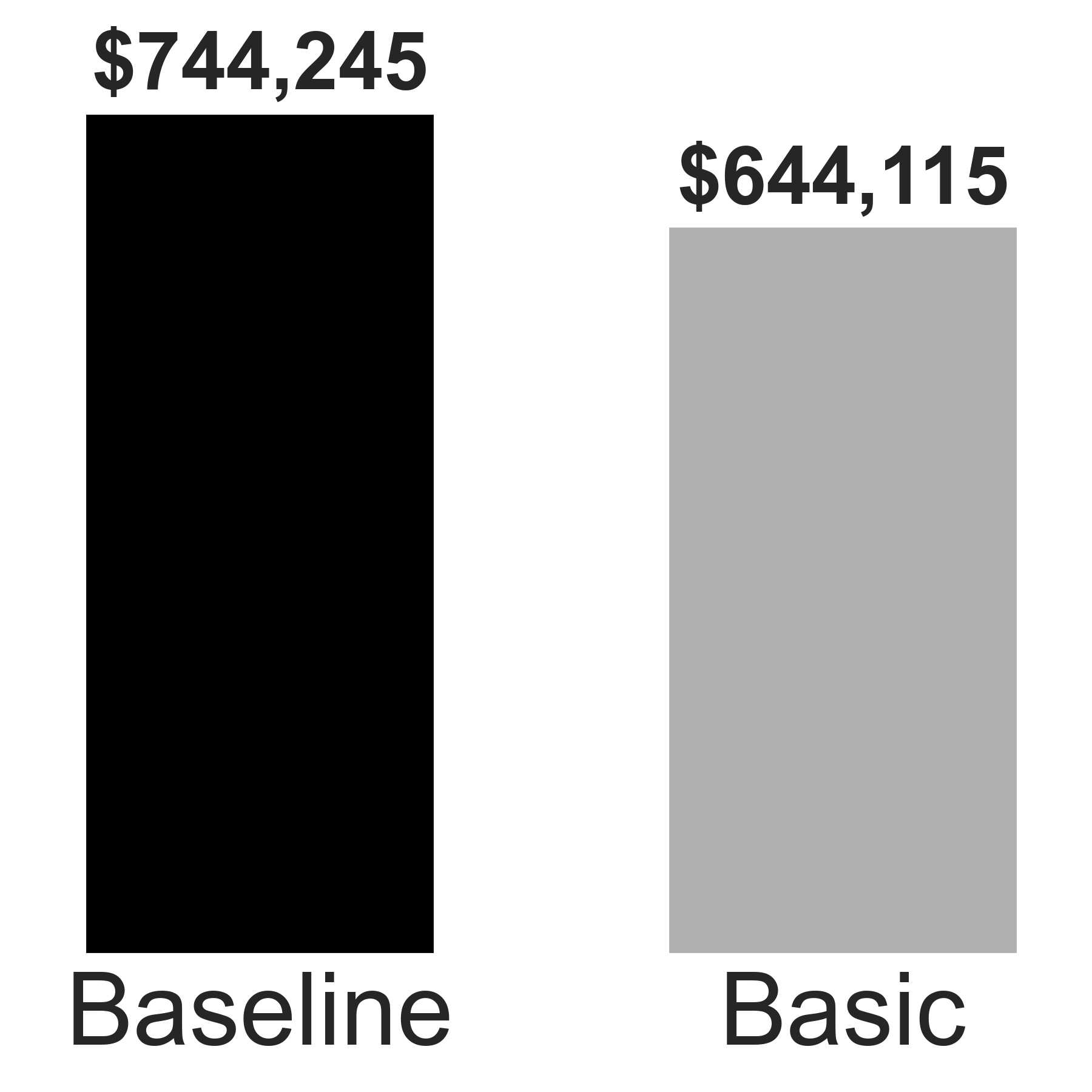

By maintaining a monthly payment of $2,218, you would incur $424,245 in interest, with a total repayment of $744,245. Your loan would be fully paid off in 28y 0mo in January 2053. Now, let's explore the payment alternatives proposed by Fynia.

2. Overview of payment alternatives

We’ll take a look at the monthly payments for each option and then check out the benefits you can get.

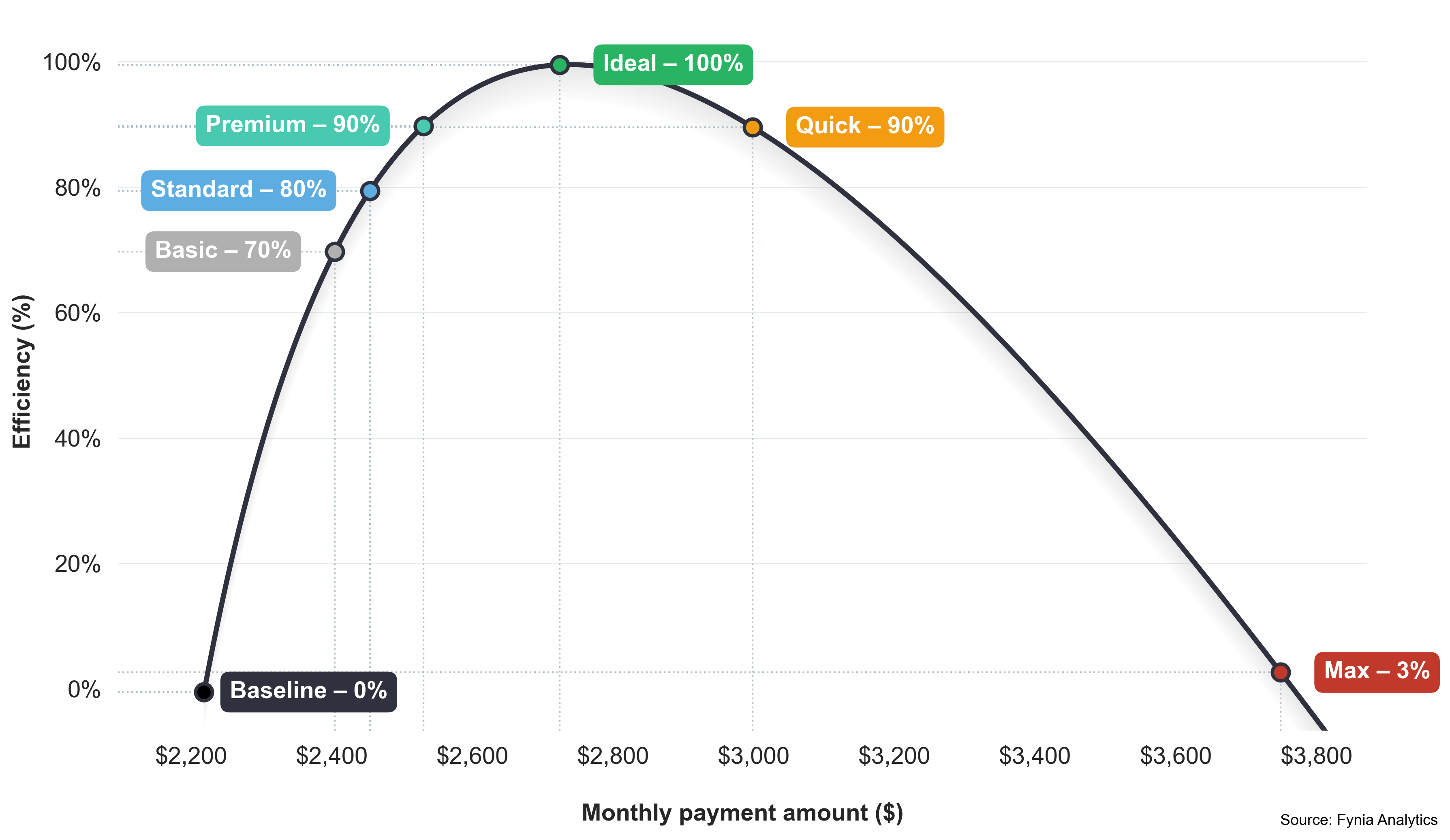

Payment Efficiency

Payment efficiency helps you get more from every installment. The chart below is tailored to your loan and shows how efficiency changes as monthly payments increase. Fynia’s suggested options help you pay smarter, balancing monthly cost with total interest saved.

Loan Optimization: Payment Efficiency vs Monthly Payment

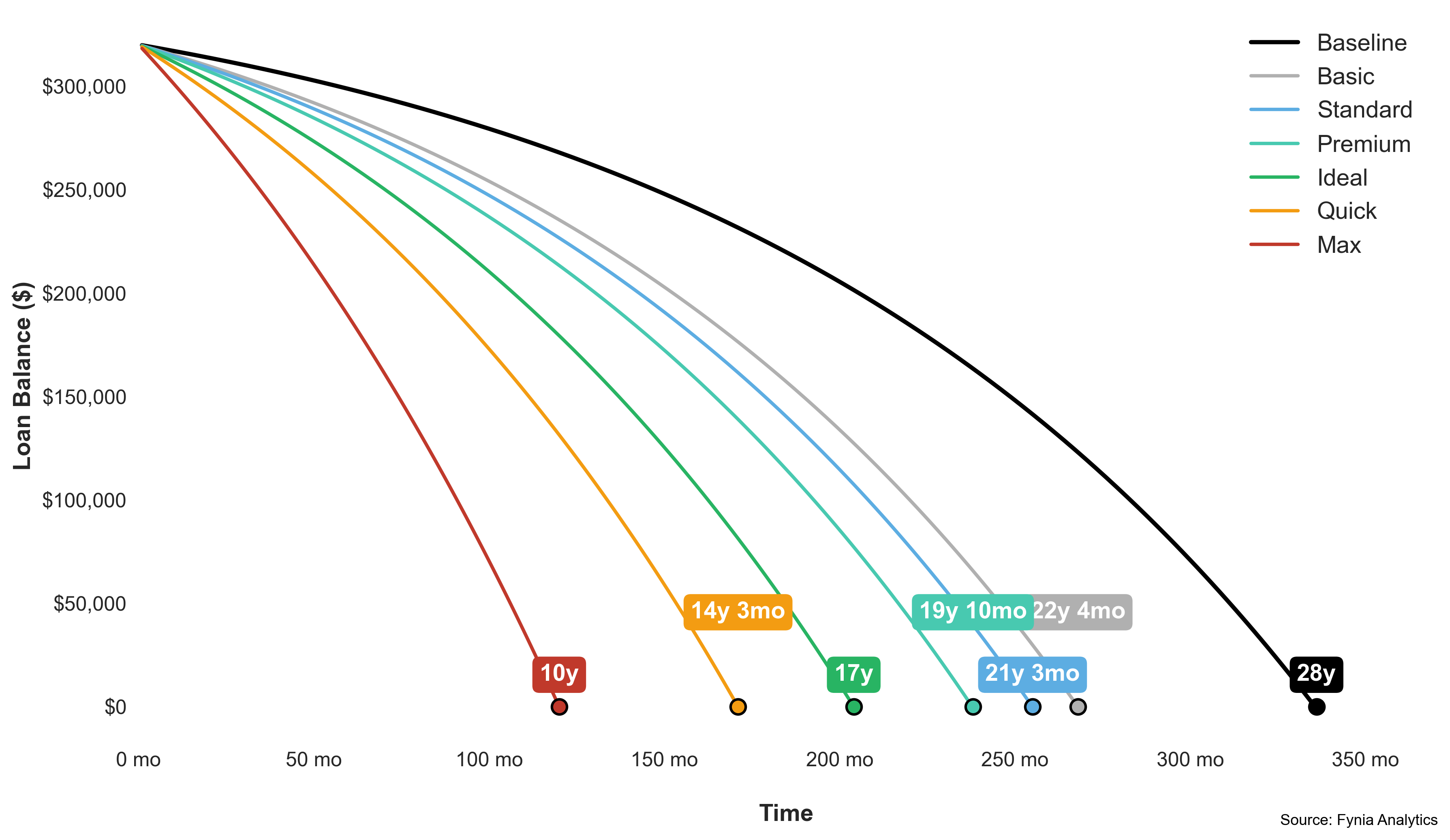

Loan Balance vs Time

Explore personalized monthly payment alternatives tailored to your loan — from the Basic plan (70% efficiency) to the Ideal plan (100%) — so you can find the perfect balance between savings and affordability.

Basic

The Budget Choice

$2,404/mo

+$186 per month

8.4% increase

Interest

$324,115

Savings: $100,130

23.6% decrease

Loan Term

22y 4mo

5y 8mo shorter

20.2% decrease

Total Repayment Amount

$644,115

The Basic option keeps your monthly payment increase to a minimum, offering modest savings in interest and a slight reduction in loan term. It’s a sensible starting point for those working with a tighter budget.

Rating

GOOD

Payment Efficiency

Standard

The Value Pick

$2,454/mo

+$236 per month

10.6% increase

Interest

$305,627

Savings: $118,618

28.0% decrease

Loan Term

21y 3mo

6y 9mo shorter

24.1% decrease

Total Repayment Amount

$625,627

The Standard option provides a balanced middle ground—more savings and faster payoff than Basic, but still very budget-friendly. It’s the best value choice for most users, combining meaningful efficiency with affordability.

Rating

VERY GOOD

Payment Efficiency

Interest

$281,626

Savings: $142,619

33.6% decrease

Loan Term

19y 10mo

8y 2mo shorter

29.2% decrease

Total Repayment Amount

$601,626

Premium increases your monthly payment modestly to achieve substantial interest savings and a shortened loan term. It offers a well-balanced upgrade in efficiency for borrowers seeking noticeable benefits without dramatic cost increases.

Rating

GREAT

Payment Efficiency

Ideal

The Best Choice

$2,724/mo

+$506 per month

22.8% increase

Interest

$235,657

Savings: $188,588

44.5% decrease

Loan Term

17y 0mo

11y 0mo shorter

39.3% decrease

Total Repayment Amount

$555,657

The Ideal option comes with a slightly higher monthly payment but delivers impeccable 100% efficiency, ensuring every cent is fully utilized to reduce both interest and your loan term.

Rating

PERFECT

Payment Efficiency

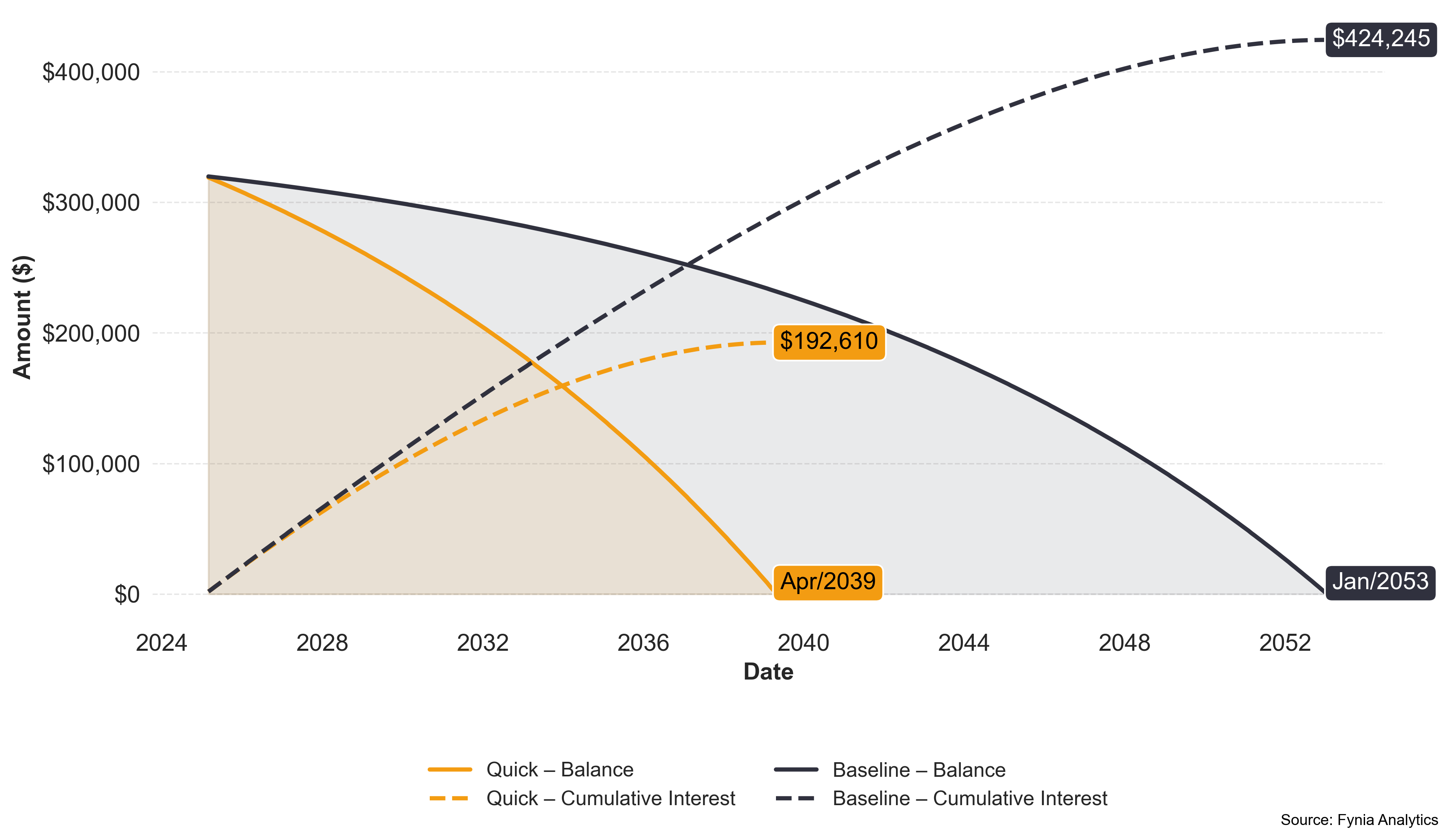

Quick

The Fast Track

$2,998/mo

+$780 per month

35.2% increase

Interest

$192,610

Savings: $231,636

54.6% decrease

Loan Term

14y 3mo

13y 9mo shorter

49.1% decrease

Total Repayment Amount

$512,610

Quick accelerates your loan payoff with a higher monthly payment, offering notable time savings. However, it’s less efficient than Ideal. If fast repayment isn't essential, Ideal is the wiser pick.

Rating

VERY GOOD

Payment Efficiency

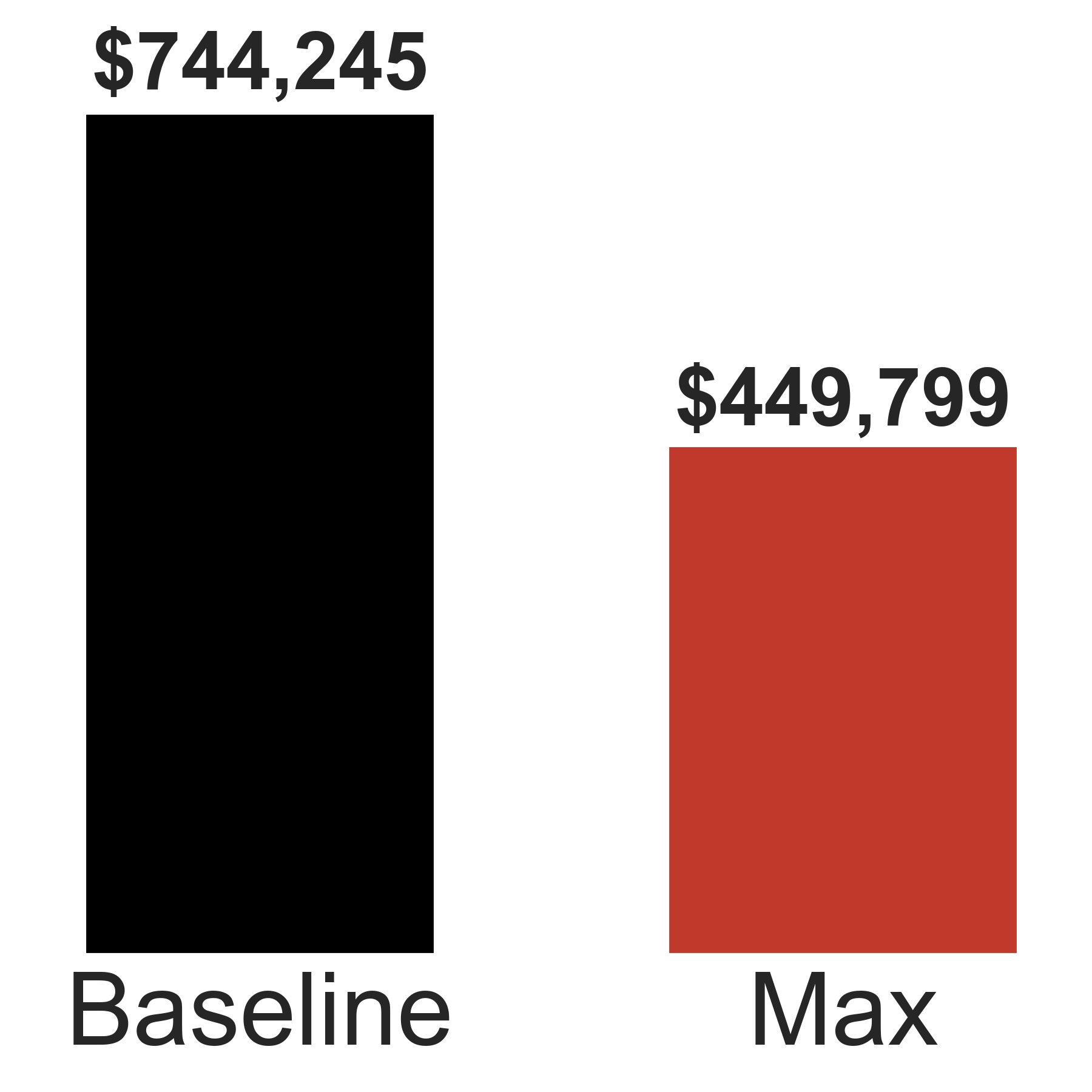

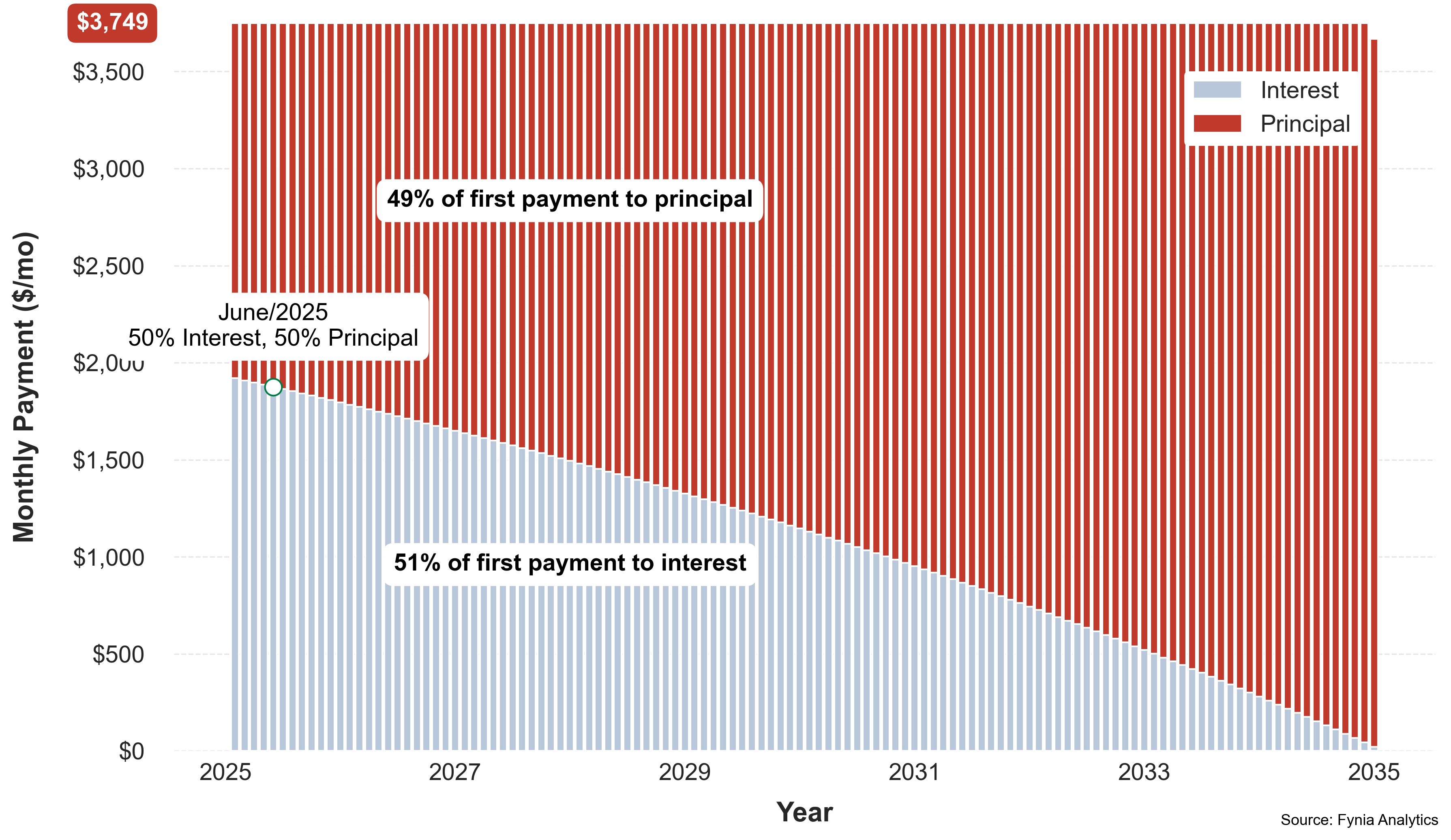

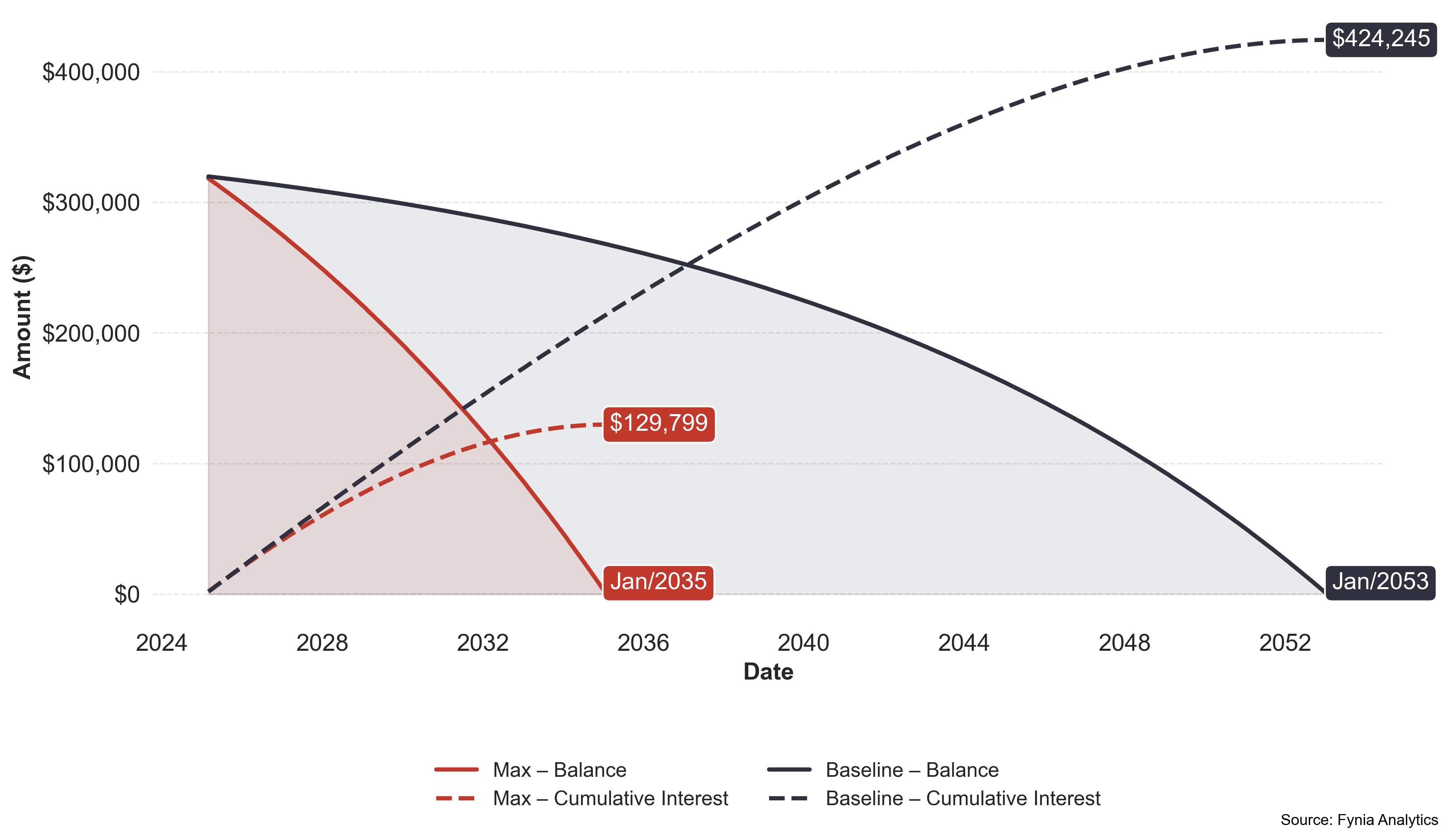

Max

The Overpay Zone

$3,749/mo

+$1,531 per month

69.0% increase

Interest

$129,800

Savings: $294,446

69.4% decrease

Loan Term

10y 0mo

18y 0mo shorter

64.3% decrease

Total Repayment Amount

$449,800

The Max option sets the upper limit for monthly payments. Beyond this point, additional increases result in negative efficiency. It serves as a clear warning: even if you can afford extra payments, going past this cap isn’t a smart strategy.

Rating

POOR

Payment Efficiency

3. In-Depth option analysis

Dive deeper into each alternative with detailed insights on the pros and cons of every option

Basic

The Budget Choice

The Basic option offers a minimal increase in monthly payments while providing moderate interest savings and a shorter loan term. It's a practical choice in scenarios where budget flexibility is limited.

Monthly Payment

$2,404

Interest To Pay

$324,115

Loan Term

22y 4mo

Total Repayment

$644,115

Baseline: $744,245

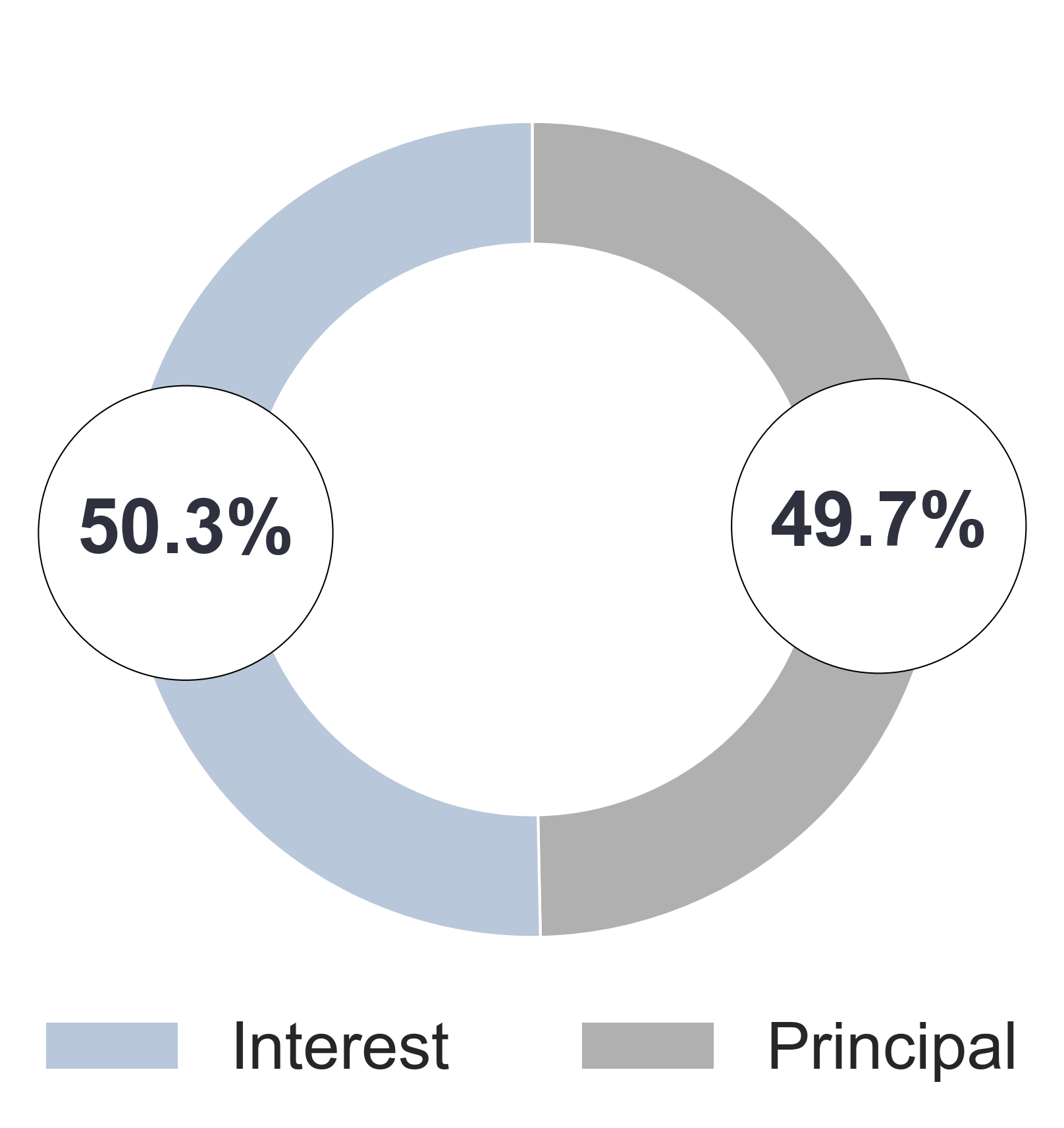

Total Payable Split

Total Payable

Monthly Payment Composition

Interest-Dominant Payment Period

57.1%

Baseline: 65.5%

lower is better

Average Principal Contribution Percentage

49.7%

Baseline: 43.0%

higher is better

Total Payment Ratio

201.3%

Baseline: 232.6%

lower is better

Balance And Cumulative Interest

50% of Balance Repaid

November/2037

Baseline: June/2043

Final Loan Payment Date

May/2047

Baseline: January/2053

Final payment (last installment)

$2,247.38

Summary

The Basic option is calibrated to target about 70% efficiency in repayment—keeping the payment increase as low as possible at 8.4%—while still delivering a 23.6% reduction in interest and a 20.2% shorter term. That’s a +70.5 pp advantage (interest reduction minus payment increase) versus Baseline. In dollar terms, a modest $186/mo unlocks about $100,130 in interest savings and trims roughly 5y 8mo from the schedule—making Basic a smart, budget-friendly starting point.

Efficiency

Normalized 0–100 based on your scenario.

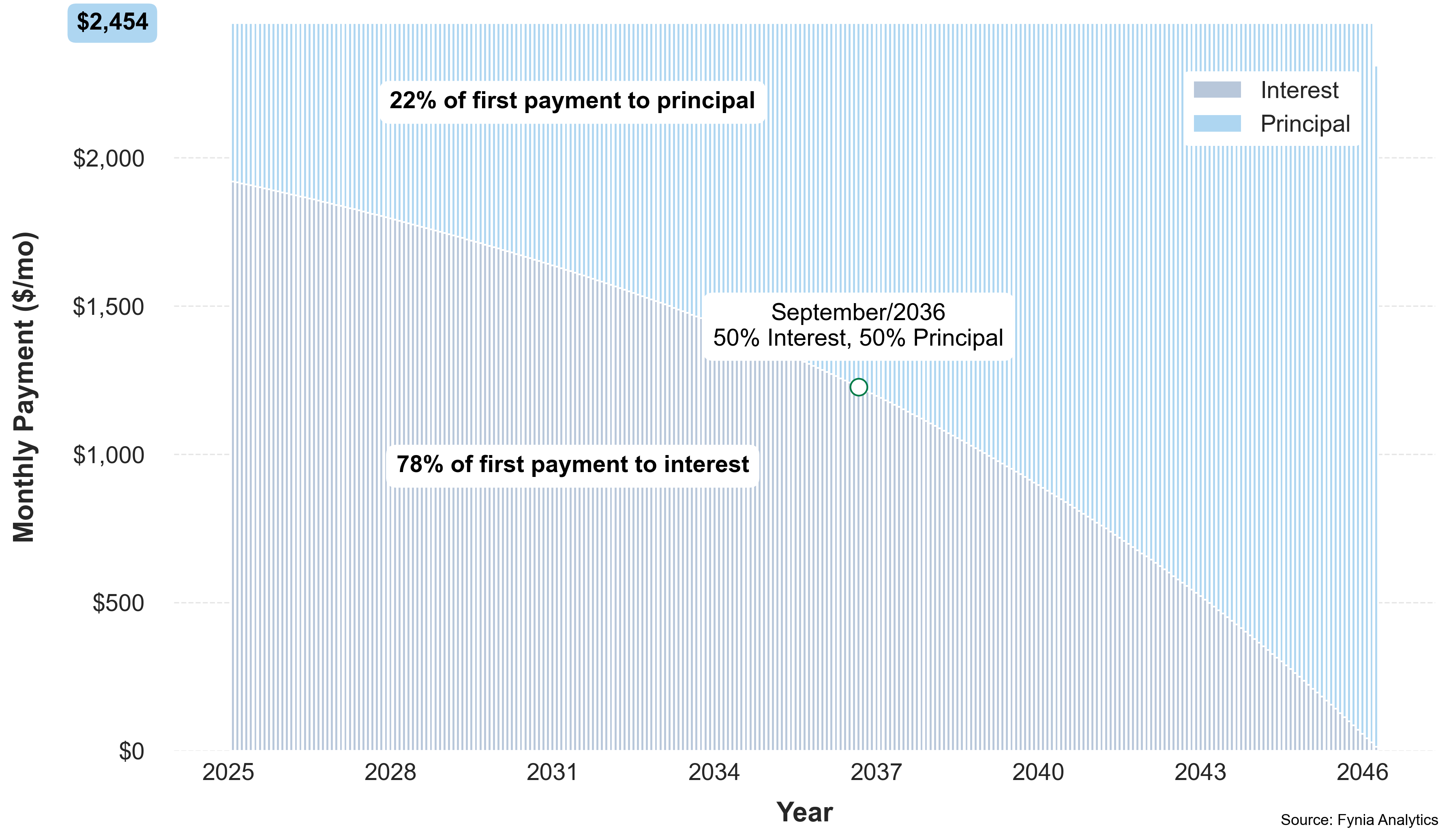

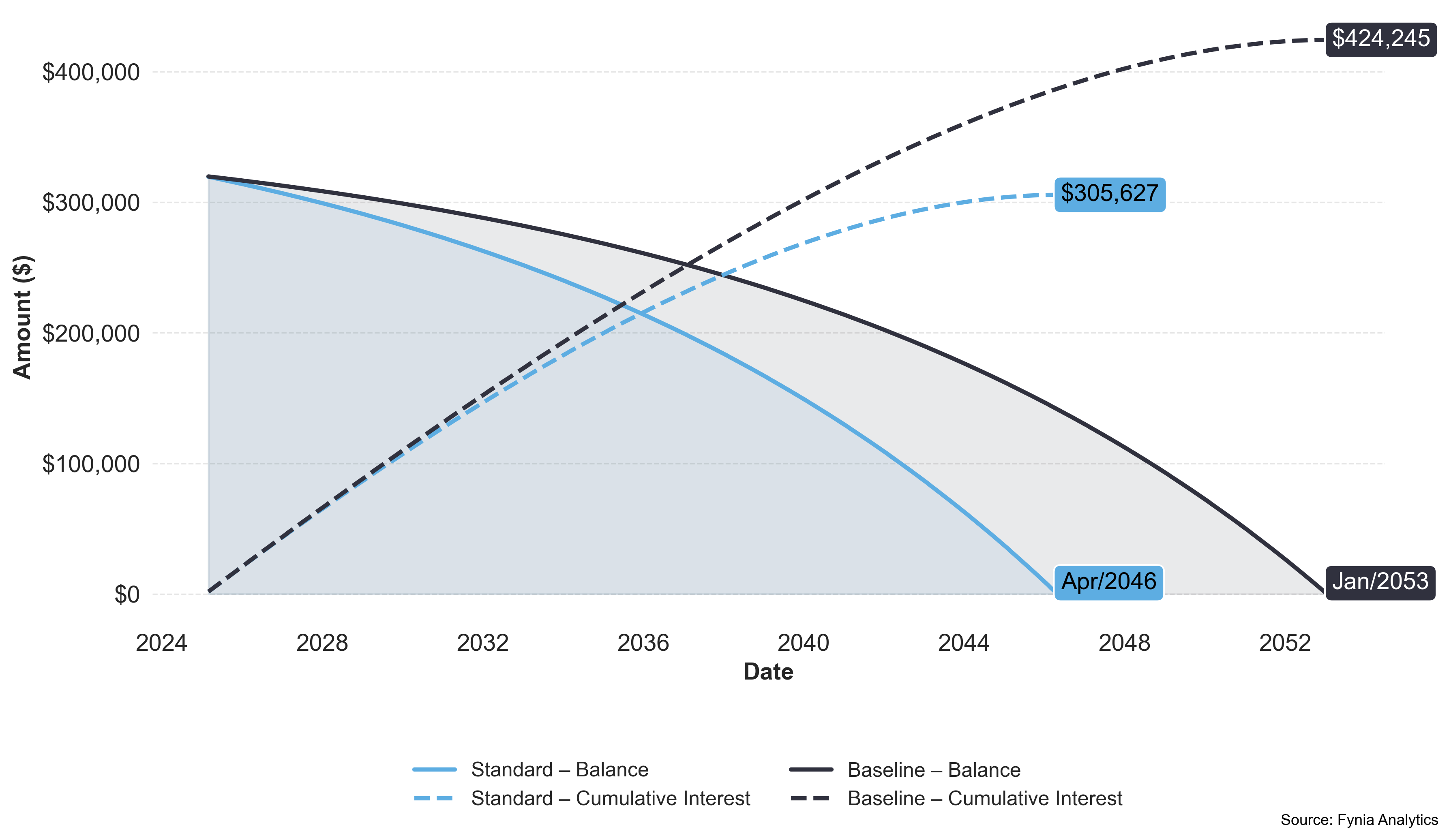

Standard

The Value Pick

The Standard option provides a balanced middle ground—more savings and faster payoff than Basic, but still very budget-friendly. It’s the best value choice for most users, combining meaningful efficiency with affordability.

Monthly Payment

$2,454

Interest To Pay

$305,627

Loan Term

21y 3mo

Total Repayment

$625,627

Baseline: $744,245

Total Payable Split

Total Payable

Monthly Payment Composition

Interest-Dominant Payment Period

54.9%

Baseline: 65.5%

lower is better

Average Principal Contribution Percentage

51.2%

Baseline: 43.0%

higher is better

Total Payment Ratio

195.5%

Baseline: 232.6%

lower is better

Balance And Cumulative Interest

50% of Balance Repaid

October/2036

Baseline: June/2043

Final Loan Payment Date

April/2046

Baseline: January/2053

Final payment (last installment)

$2,311.03

Summary

The Standard option is tuned toward roughly 80% efficiency—a balanced, best-value step up from Basic. A 10.6% increase in the monthly payment delivers a 28.0% reduction in interest and a 24.1% shorter term—yielding a +17.4 pp advantage (interest reduction minus payment increase) vs Baseline. In dollar terms, that’s +$236/mo to save about $118,618 and trim 6y 9mo from the schedule.

Efficiency

Normalized 0–100 based on your scenario.

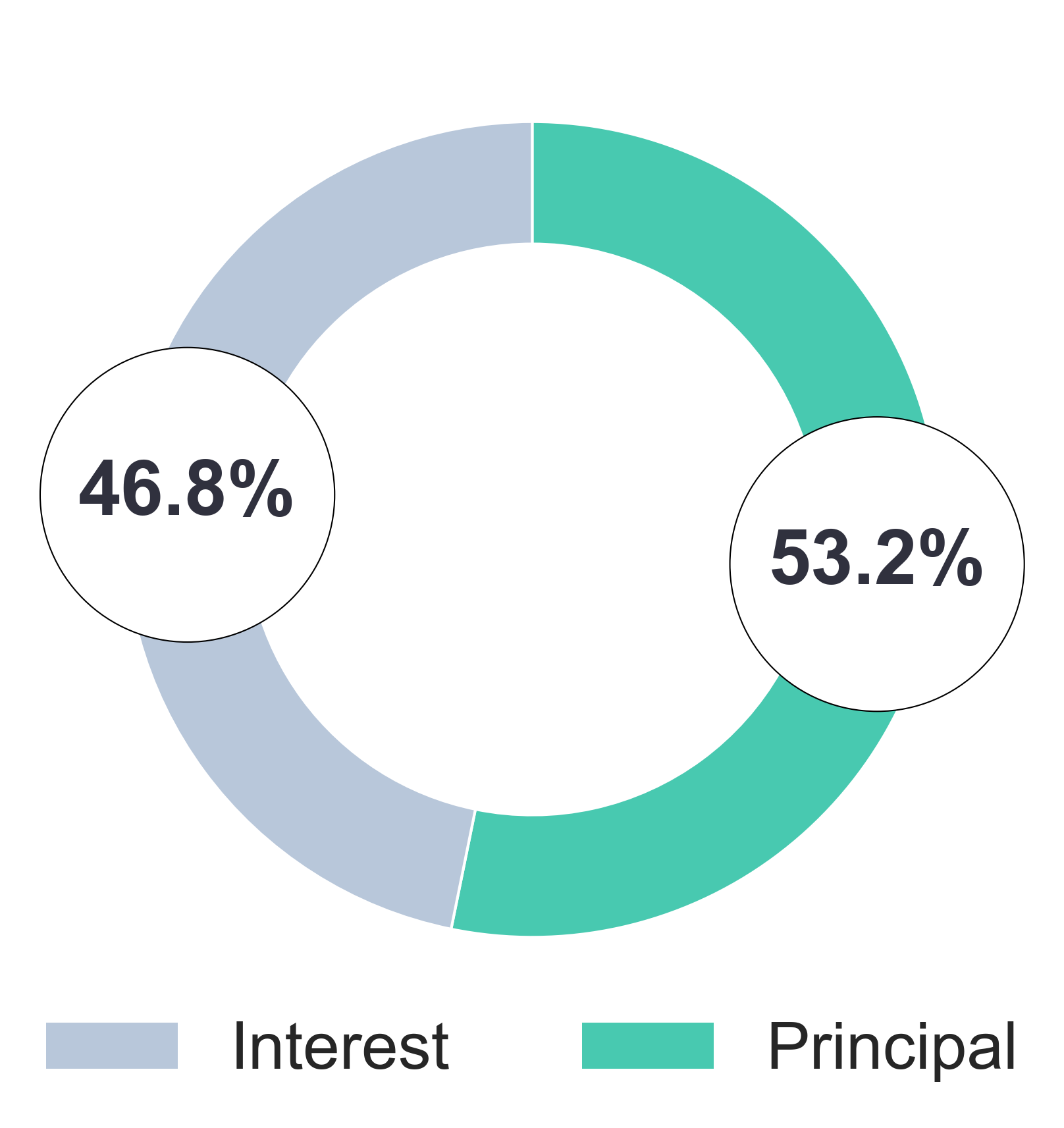

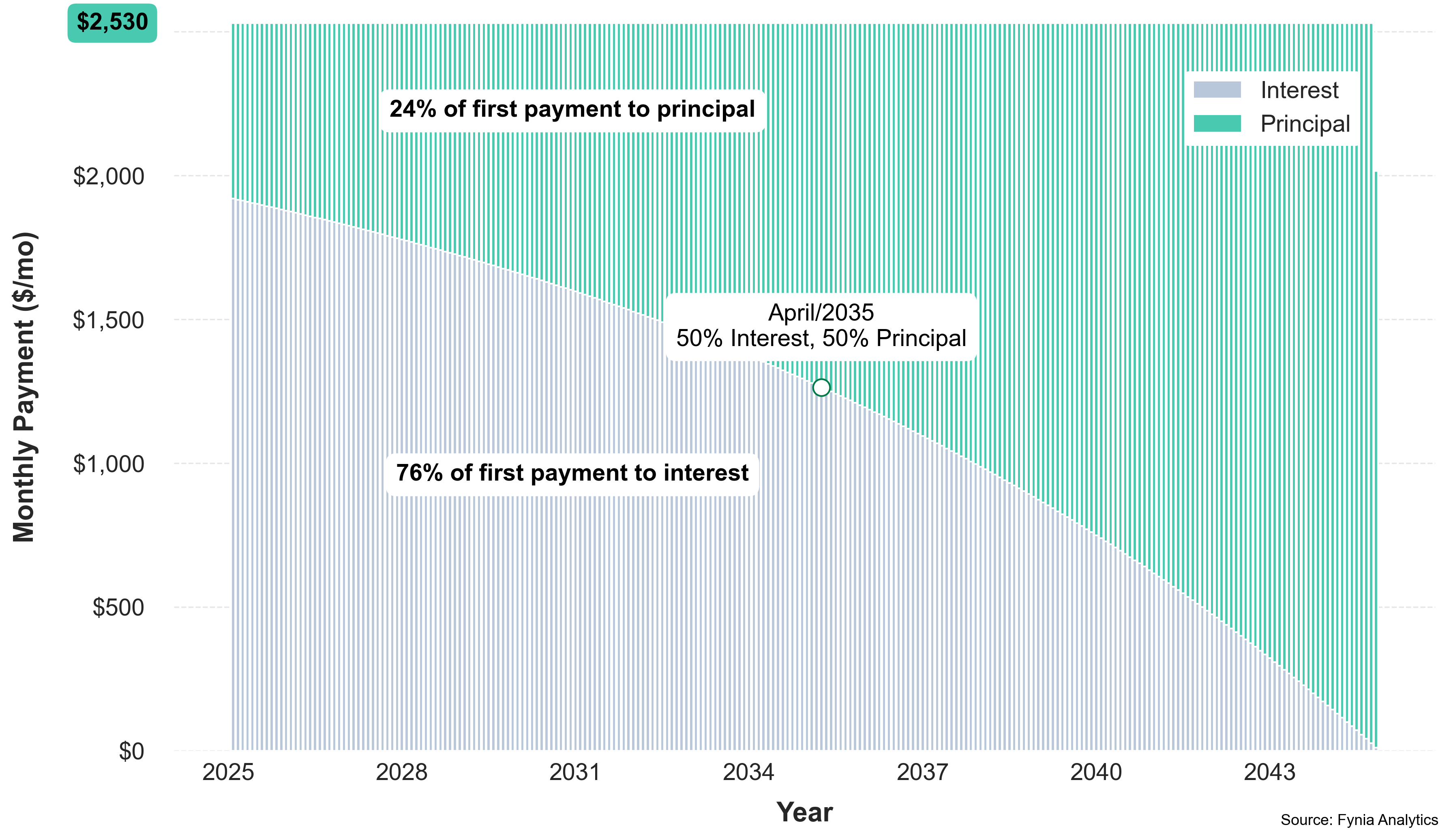

$2,530

$281,626

19y 10mo

$601,626

Baseline: $744,245

Total Payable Split

Total Payable

Monthly Payment Composition

Interest-Dominant Payment Period

51.3%

Baseline: 65.5%

lower is better

Average Principal Contribution Percentage

53.2%

Baseline: 43.0%

higher is better

Total Payment Ratio

188.0%

Baseline: 232.6%

lower is better

Balance And Cumulative Interest

50% of Balance Repaid

April/2035

Baseline: June/2043

Final Loan Payment Date

November/2044

Baseline: January/2053

Final payment (last installment)

$2,016.34

Summary

The Premium option targets roughly 90% efficiency—a meaningful step up from Standard while keeping costs contained. A 14.1% increase in the monthly payment delivers a 33.6% reduction in interest and a 29.2% shorter term—yielding a +19.5 pp advantage (interest reduction minus payment increase) vs Baseline. In dollar terms, that’s $312/mo to save about $142,619 and cut 8y 2mo from the schedule—making Premium a powerful yet competitively priced choice.

Efficiency

Normalized 0–100 based on your scenario.

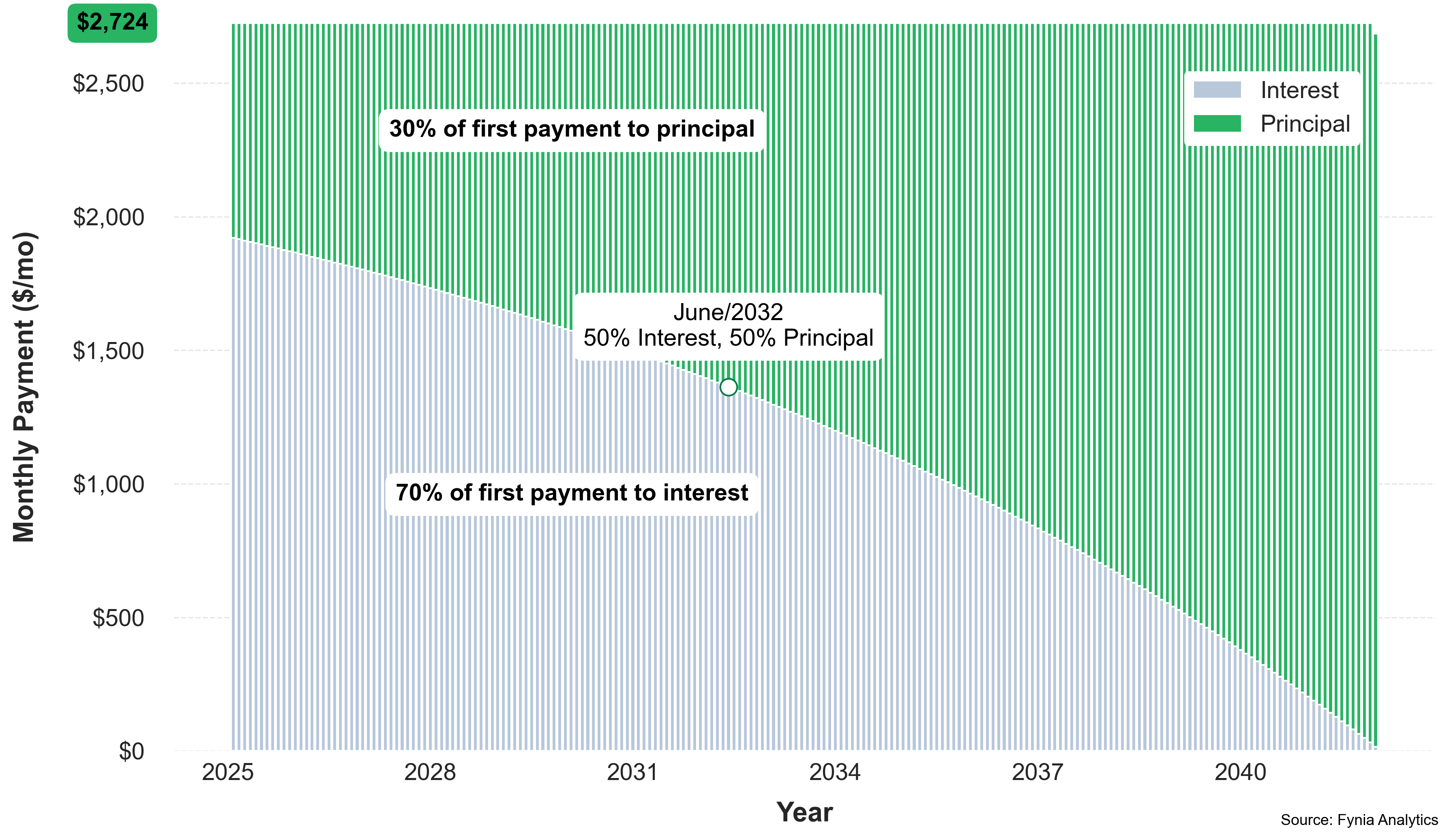

Ideal

The Best Choice

The Ideal option involves a slightly higher monthly payment but achieves perfect 100% efficiency, ensuring every cent is fully utilized to reduce both interest and the loan term.

Monthly Payment

$2,724

Interest To Pay

$235,657

Loan Term

17y 0mo

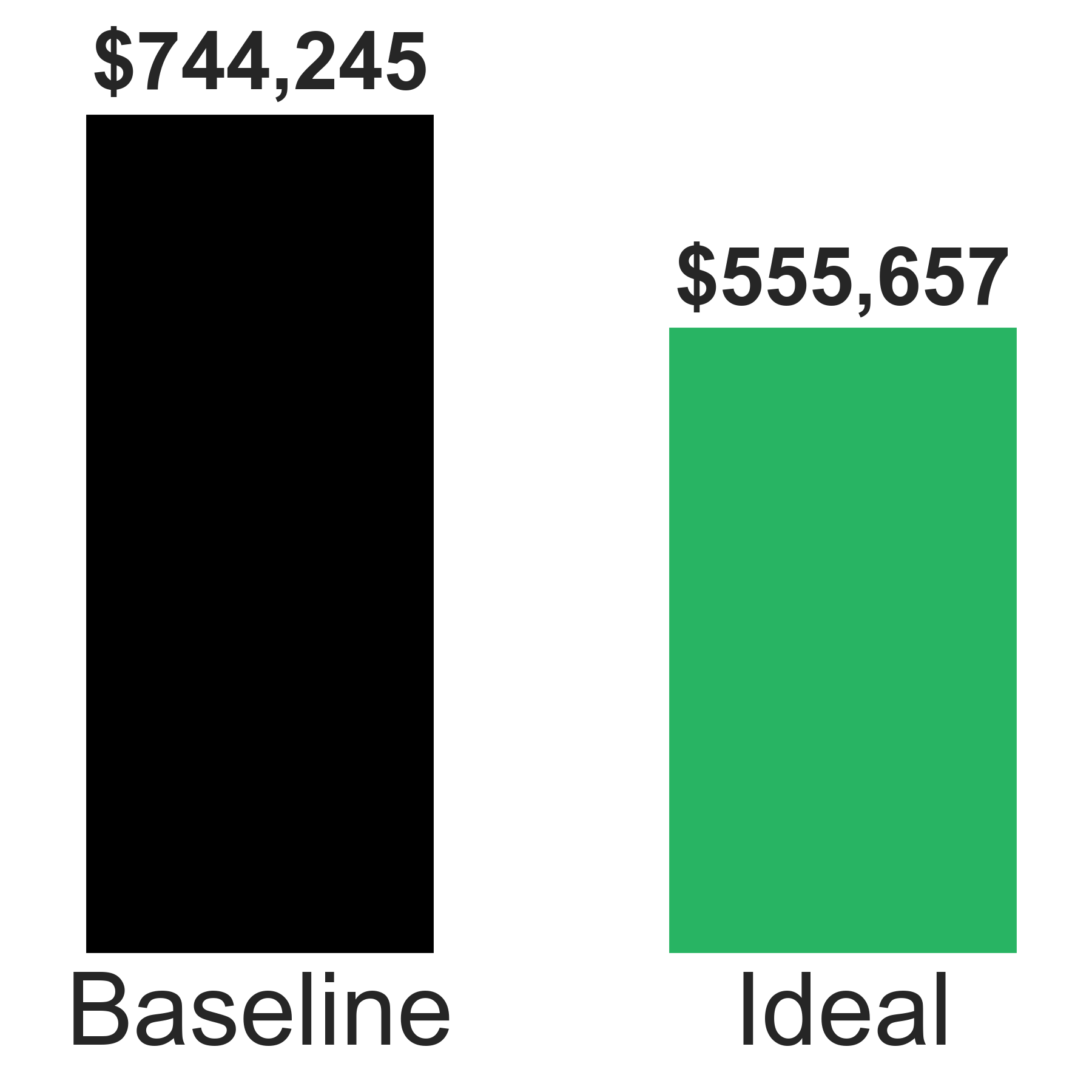

Total Repayment

$555,657

Baseline: $744,245

Total Payable Split

Total Payable

Monthly Payment Composition

Interest-Dominant Payment Period

43.6%

Baseline: 65.5%

lower is better

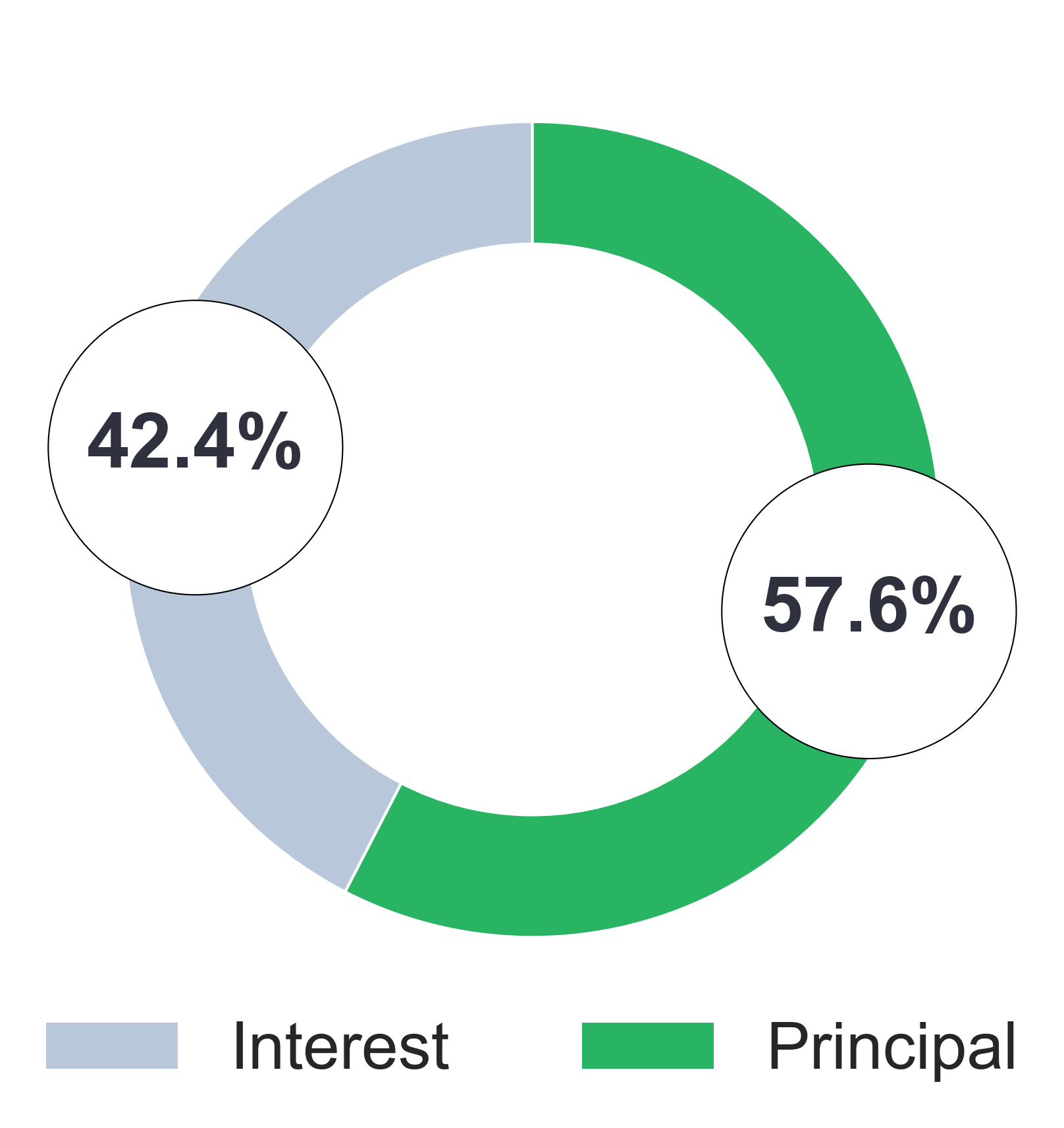

Average Principal Contribution Percentage

57.6%

Baseline: 43.0%

higher is better

Total Payment Ratio

173.6%

Baseline: 232.6%

lower is better

Balance And Cumulative Interest

50% of Balance Repaid

July/2032

Baseline: June/2043

Final Loan Payment Date

January/2042

Baseline: January/2053

Final payment (last installment)

$2,685.31

Summary

The Ideal option pursues 100% efficiency—every extra dollar works fully toward cutting interest and time. A 22.8% increase in the monthly payment translates into a 44.5% reduction in interest and a 39.3% shorter term—yielding a +21.7 pp advantage (interest reduction minus payment increase) vs Baseline. In dollar terms, that’s $506/mo to save about $188,588 and cut 11y 0mo from the schedule—making Ideal the mathematically optimal choice for unparalleled efficiency.

Efficiency

Normalized 0–100 based on your scenario.

Quick

The Fast Track

Quick accelerates loan payoff with a higher monthly payment, offering significant time savings. However, it is less efficient than the Ideal option—if fast repayment isn’t essential, the Ideal choice is more effective.

Monthly Payment

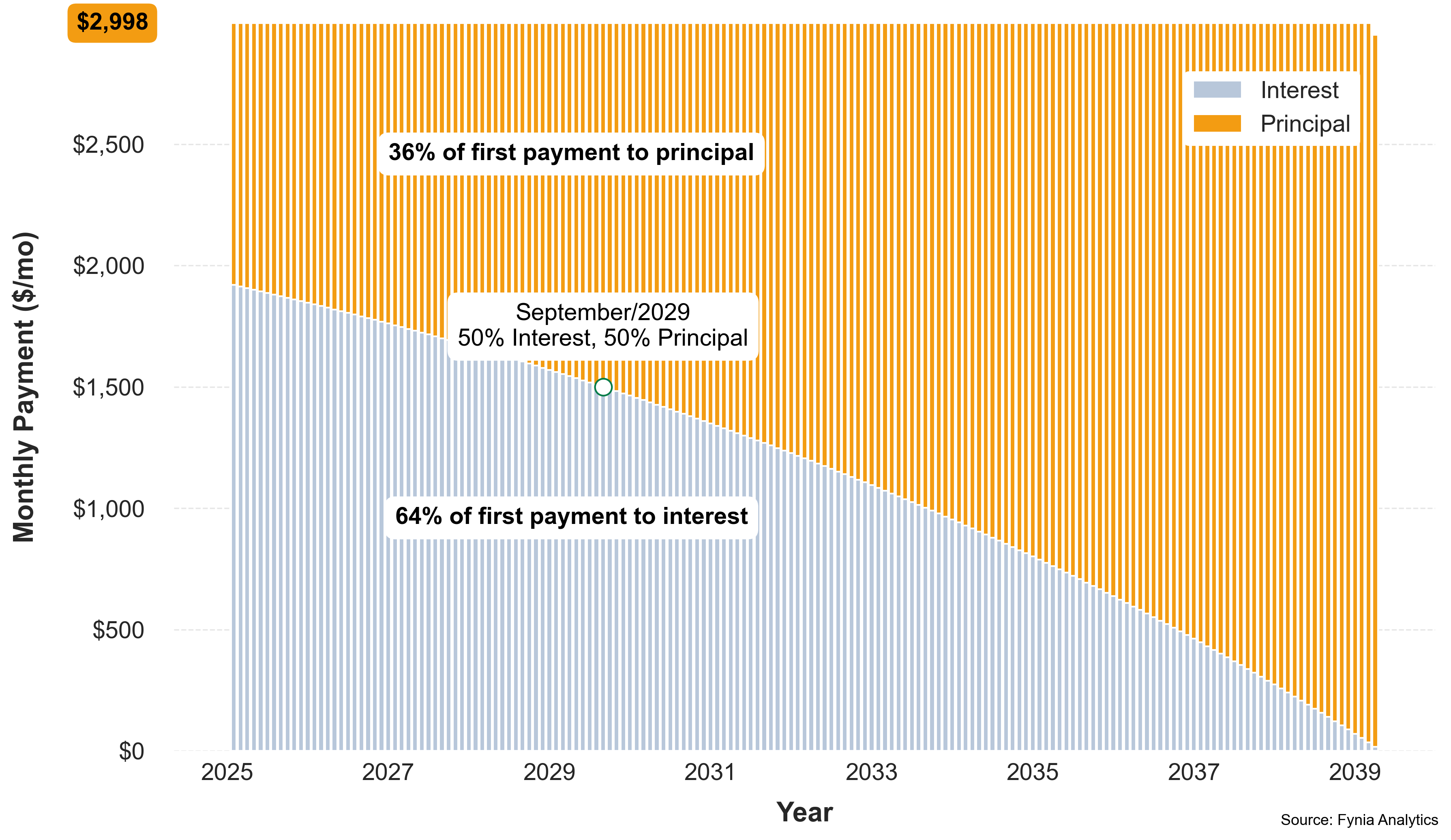

$2,998

Interest To Pay

$192,610

Loan Term

14y 3mo

Total Repayment

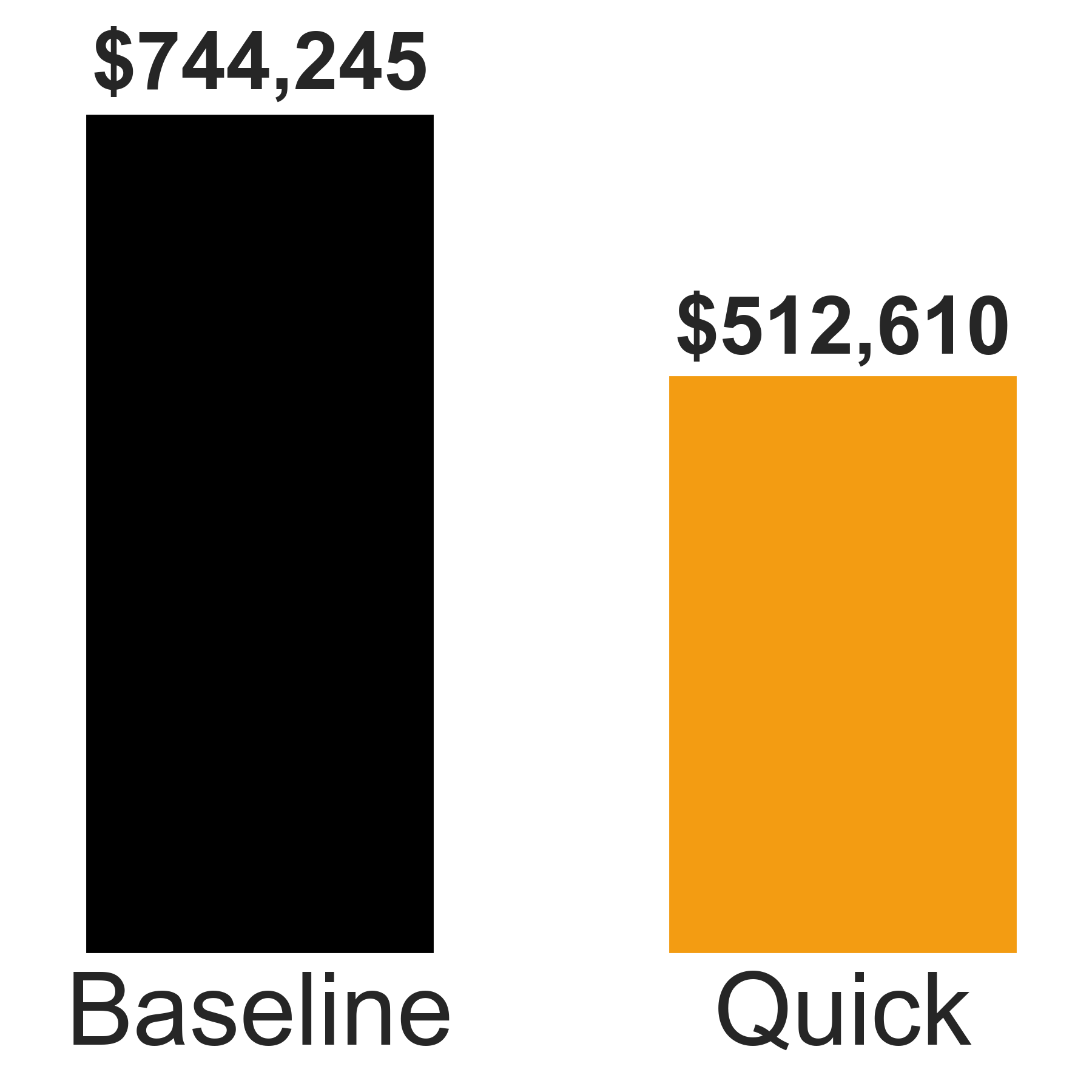

$512,610

Baseline: $744,245

Total Payable Split

Total Payable

Monthly Payment Composition

Interest-Dominant Payment Period

32.8%

Baseline: 65.5%

lower is better

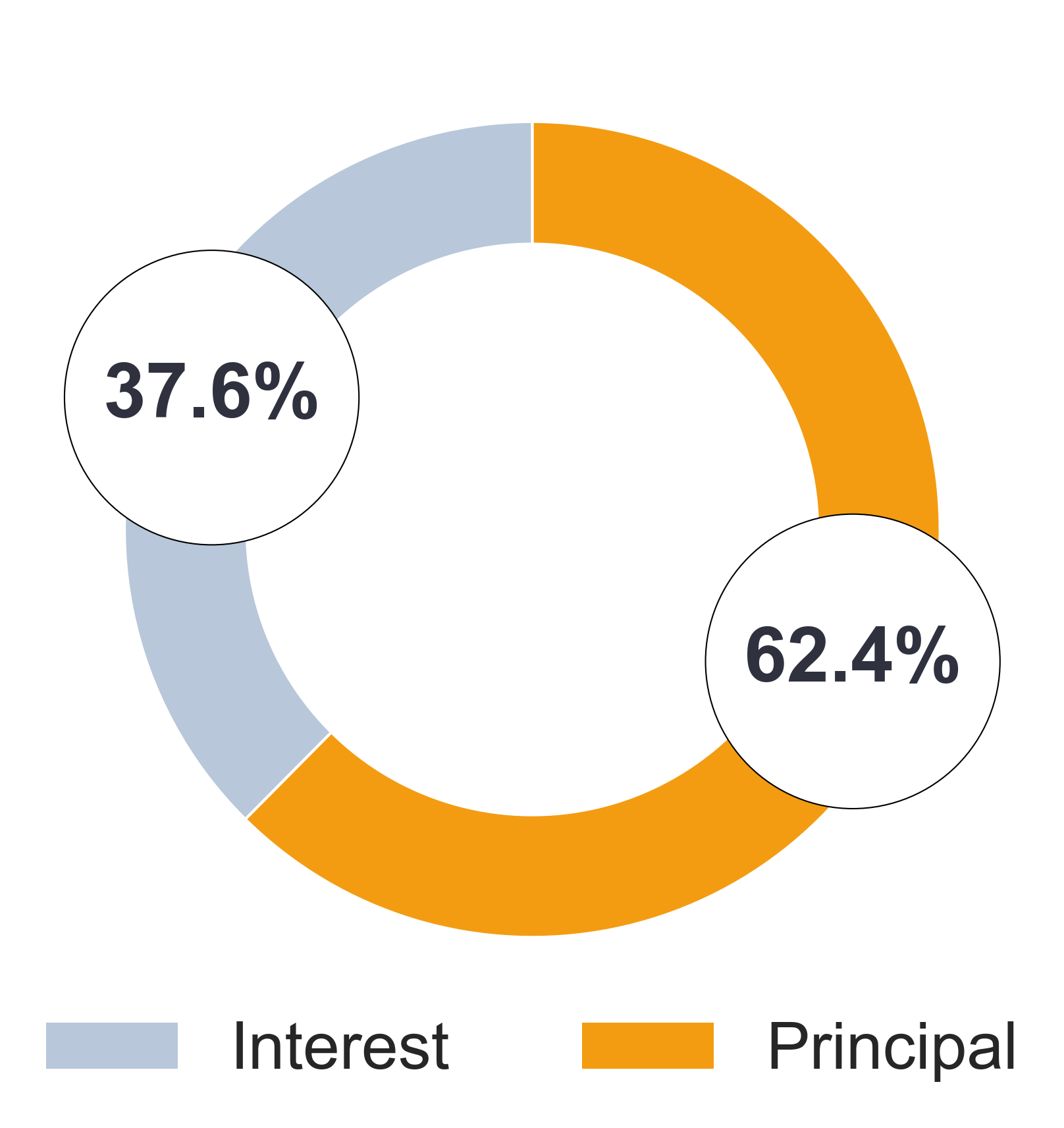

Average Principal Contribution Percentage

62.4%

Baseline: 43.0%

higher is better

Total Payment Ratio

160.2%

Baseline: 232.6%

lower is better

Balance And Cumulative Interest

50% of Balance Repaid

October/2029

Baseline: June/2043

Final Loan Payment Date

April/2039

Baseline: January/2053

Final payment (last installment)

$2,949.86

Summary

The Quick option prioritizes speed: a 35.2% increase in the monthly payment delivers a 54.6% reduction in interest and a 49.1% shorter term—yielding a +19.4 pp advantage (interest reduction minus payment increase) vs Baseline. It sacrifices some efficiency relative to Ideal but dramatically accelerates payoff. In dollar terms, that’s $780/mo to save about $231,636 and cut 13y 9mo from the schedule—making Quick the right choice for those who value speed over maximum efficiency.

Efficiency

Normalized 0–100 based on your scenario.

Max

The Overpay Zone

The Max option represents the upper limit for monthly payments—beyond this point, additional increases lead to negative efficiency. It serves as a clear indicator that, even if extra payments are affordable, exceeding this cap is not a wise strategy.

Monthly Payment

$3,749

Interest To Pay

$129,800

Loan Term

10y 0mo

Total Repayment

$449,800

Baseline: $744,245

Total Payable Split

Total Payable

Monthly Payment Composition

Interest-Dominant Payment Period

4.2%

Baseline: 65.5%

lower is better

Average Principal Contribution Percentage

71.1%

Baseline: 43.0%

higher is better

Total Payment Ratio

140.6%

Baseline: 232.6%

lower is better

Balance And Cumulative Interest

50% of Balance Repaid

July/2025

Baseline: June/2043

Final Loan Payment Date

January/2035

Baseline: January/2053

Final payment (last installment)

$3,668.50

Summary

The Max option pushes the monthly payment to a practical ceiling: a 69.0% increase delivers a 69.4% reduction in interest and a 64.3% shorter term—yielding a +0.4 pp advantage (interest reduction minus payment increase) vs Baseline. In nominal terms, that’s $1,531/mo to save about $294,446 and cut 18y 0mo from the schedule. Note: treat Max as an upper boundary—going beyond this level reduces overall efficiency and can turn negative.

Efficiency

Normalized 0–100 based on your scenario.

4. Payment Alternative Navigator

Review the table below to compare each option’s efficiency and affordability. The goal is to select the alternative that maximizes savings in interest and time while remaining comfortably within the budget for the entire loan term.

|

Baseline

$2,218 /mo

|

Basic

$2,404 /mo

+$186

8.4% increase |

Standard

$2,454 /mo

+$236

10.6% increase |

$2,530 /mo

+$312

14.1% increase |

Ideal

$2,724 /mo

+$506

22.8% increase |

Quick

$2,998 /mo

+$780

35.2% increase |

Max

$3,749 /mo

+$1,531

69.0% increase |

|

| Rank Order | - | 4th | 3rd | 2nd | 1st | - | - |

| Interest |

$424,245

|

$324,115

$100,130 savings

23.6% decrease |

$305,627

$118,618 savings

28.0% decrease |

$281,626

$142,619 savings

33.6% decrease |

$235,657

$188,588 savings

44.5% decrease |

$192,610

$231,636 savings

54.6% decrease |

$129,800

$294,446 savings

69.4% decrease |

| Loan Term |

28y 0mo

|

22y 4mo

5y 8mo shorter

20.2% decrease |

21y 3mo

6y 9mo shorter

24.1% decrease |

19y 10mo

8y 2mo shorter

29.2% decrease |

17y 0mo

11y 0mo shorter

39.3% decrease |

14y 3mo

13y 9mo shorter

49.1% decrease |

10y 0mo

18y 0mo shorter

64.3% decrease |

| Total Repayment | $744,245 | $644,115 | $625,627 | $601,626 | $555,657 | $512,610 | $449,800 |

| Efficiency Ratio | - | 15.2 | 17.3 | 19.6 | 21.6 | 19.4 | 0.4 |

| Payment Efficiency | 0.0% | 70.5% | 80.1% | 89.9% | 100% | 89.9% | 2.7% |

5. Download PDF Report

Thank you for trusting Fynia! Download your PDF report for easy access to all the details of your loan analysis. Whether it's a quick review or an in-depth look, this report will help you make better financial decisions.

With all the loan details in front of him, Joe can confidently choose the best monthly payment plan.